Medical expenses can be difficult to pay off, especially if you find yourself going back and forth to a hospital or clinic. Sometimes, health insurance isn’t enough either, which makes health savings accounts a great alternative. Health savings accounts (HSAs) can offer huge and life-changing benefits, especially as you get close to retirement. This article will tell you what you need to know.

What Is a Health Savings Account?

A health savings account lets people covered under a high-deductible health plan (HDHP) save for qualified medical expenses. It helps you prepare for health care costs, which can be beneficial as you age. Unlike other savings accounts, HSA offers tax advantages, rollovers, investment opportunities and multiperson contributions. You only need to meet the eligibility requirements to open an account.

Health Savings Accounts vs. Health Insurance

Health savings accounts are savings accounts, meaning they help you save for potential medical costs. Health insurance helps you cover the cost as the insurer pays a portion of the bill, as long as you pay the monthly premium.

An HDHP is a health insurance plan. It typically has larger annual deductibles than other health plans, so it’s best for healthier individuals who don’t need much coverage. A deductible is a portion you must pay out of pocket. However, HDHPs come with lower monthly premiums, which can also be attractive. Because HSAs require an HDHP, you can use both to your advantage.

How Does a Health Savings Account Work?

An HSA is a custodial account, so you must set one up with a qualified trustee. You or other qualified contributors can add money to the account, with certain limits. Plus, you can only contribute cash — no stocks or property payments allowed.

Contributions to an HSA are tax-advantaged. If your account is employer-sponsored, you can contribute pretax funds, which saves you money on taxes. You can also contribute posttax money, which is tax-deductible, but that method doesn’t save you as much.

You can use the money in your account to pay for qualified medical expenses, such as ambulatory expenses, body scans, fertility enhancement and routine care. You can read Publication 502 from the IRS for the full list. Insurance premiums aren’t generally considered qualified medical expenses.

The distributions you receive from your HSA are tax-free. You can also choose to be reimbursed for your medical expenses, as long as you’ve incurred them after you establish your account. Follow the other health savings account rules and qualifications set by the IRS for a smooth experience.

Requirements and Eligibility

To be qualified for an HSA, you:

- Need to be covered under an HDHP on the first day of the month

- Should not be enrolled in Medicare

- Have no other health coverage, unless permitted

- Are not a dependent on another person’s tax return

You can also be eligible if you’re a veteran with a disability caused by your service and you’re receiving medical care through Veterans Affairs. You also can’t open a joint HSA account with another person. Your spouse will have to open a separate account if they’re eligible.

When opening an HSA account, you don’t need authorization from the IRS. Just open one with a qualified trustee, which could be an insurance company, a bank or another entity approved by the IRS. Your HSA trustee can differ from your health plan provider. You can also open multiple HSAs, as long as you’re mindful of the contribution limits.

Contribution Guidelines

Eligible individuals can contribute to your HSA, which can include your family members and your employer. Your employer can make contributions, even if the account is yours. If you’re unemployed or self-employed, your family members or another person can contribute on your behalf. Contribution limits depend on your HDHP coverage, age and dates of eligibility and ineligibility. For 2026, the contribution limits are:

- Self-only HDDP coverage: $4,400 (includes employee + employer contributions)

- Individual with family HDPD coverage: $8,750 (includes employee + employer contributions)

- Individuals aged 55 and over: Additional $1,000 catch-up contribution per year. If both spouses are 55+ and covered under a family HDHP, you can contribute up to $10,750 total ($8,750 family limit + $1,000 catch-up each), as long as each spouse makes their catch-up contribution to their own HSA.

You need to report all HSA contributions in the Form 8889. Excess contributions are not deductible, and excess contributions from your employer will be part of your gross income. Employer contributions are considered part of the limits. You may need to reduce your contributions or those of another person if your employer’s contributions will put you over the limit.

If you rollover your money from an existing HSA to a new HSA, this is considered a rollover contribution and is not subject to the contribution limits. However, you must roll over the amount within 60 days and are limited to one rollover contribution per year.

Lastly, a health savings account is portable, so it’s yours even if you switch employers.

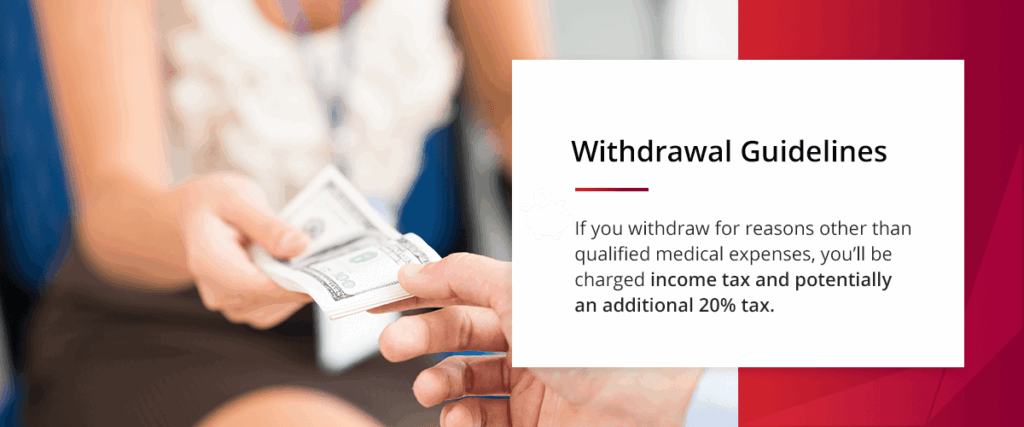

Withdrawal Guidelines

The money you get from your health savings account is called a distribution. This includes payments with your debit card and money withdrawn by other individuals on your behalf. If you withdraw for reasons other than qualified medical expenses, you’ll be charged income tax and potentially an additional 20% tax. You don’t have to use the money in your account every year. Unused balances will be carried over to the next year.

Benefits of Opening a Health Savings Account

The main benefit of a health savings account is its triple tax advantage, but other benefits include retirement benefits and opportunities for investment.

Tax Benefits

Here’s what a triple tax advantage means:

- Tax-deductible contributions: Your contributions are deductible on your tax return. You can claim the tax deduction even without itemizing them on the Form 1040.

- Tax-free medical expenses: The distributions used for qualified medical expenses can be tax-free.

- Tax-free earnings: The interests earned in your account are also tax-free.

Note that a 6% excise tax will be charged on excess contributions. You can withdraw the excess amount to avoid paying this fee.

Retirement Benefits

An HSA offers significant benefits for your retirement because it helps you save for medical expenses in the future, when you may need it most. Because the money in your HSA carries over from year to year, it’s a great way to set a targeted goal of saving for these potential expenses. The yearly interest can also increase your savings, so the earlier you start, the better.

You can also choose a beneficiary when setting up your HSA. If you choose your spouse, it will become your spouse’s HSA after your death. Otherwise, the account will stop being an HSA and become taxable to a beneficiary based on the market value. Your estate can also be a beneficiary, and the amount will be included in your final income tax return.

Investment Options

Depending on your provider, you can allow the account holders of your HSA to invest the amount after you meet a certain threshold. You can choose from the limited set of investments your provider may offer. If investing is your priority and you’re unsatisfied with the available options, you can look for other HSA plans that have what you want.

Because the interest from an HSA is tax-free, opening an account is a great alternative or starting point for investing. It can also be significantly helpful, given that health care costs can get pricier in the future.

Is an HSA Worth It?

An HSA can be worth it, considering medical expenses can get expensive. If you’re young and healthy, you can make the most out of it by starting early. Starting early can help you take advantage of the tax-free earnings while saving more for retirement. Unlike other savings accounts, an HSA also enables you to set targeted goals. You won’t mix up your savings with other potential expenses, such as rent or vacation.

Accuplan Offers Competitive Health Savings Accounts

Accuplan Benefits Services is a leader in the industry, helping people since 1985. If you choose our HSA account, you’ll get complete control and have it personalized to your needs. You’ll also get low fees, an easy self-reimbursement process and fully dedicated customer support. Our competitive rates ensure that your money works well for you, too. Open an account today to get started.

Disclaimer: Our information shouldn’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.