Setting up a self-directed IRA is a great way to take control of your retirement funds by investing in assets like real estate, gold and other options. The IRS has outlined several rules regarding investing in an IRA or 401k, including the disqualified persons rule.

In short, a disqualified person is anyone in a position to exercise substantial influence before the benefitting transaction. In other words, anyone with power, responsibility or interest in an organization can only benefit from or take out funds after retirement. In the same way, an individual cannot invest their funds into a family member’s rental property or other organization.

For more information on this topic, please reference Publication 560 on the IRS website.

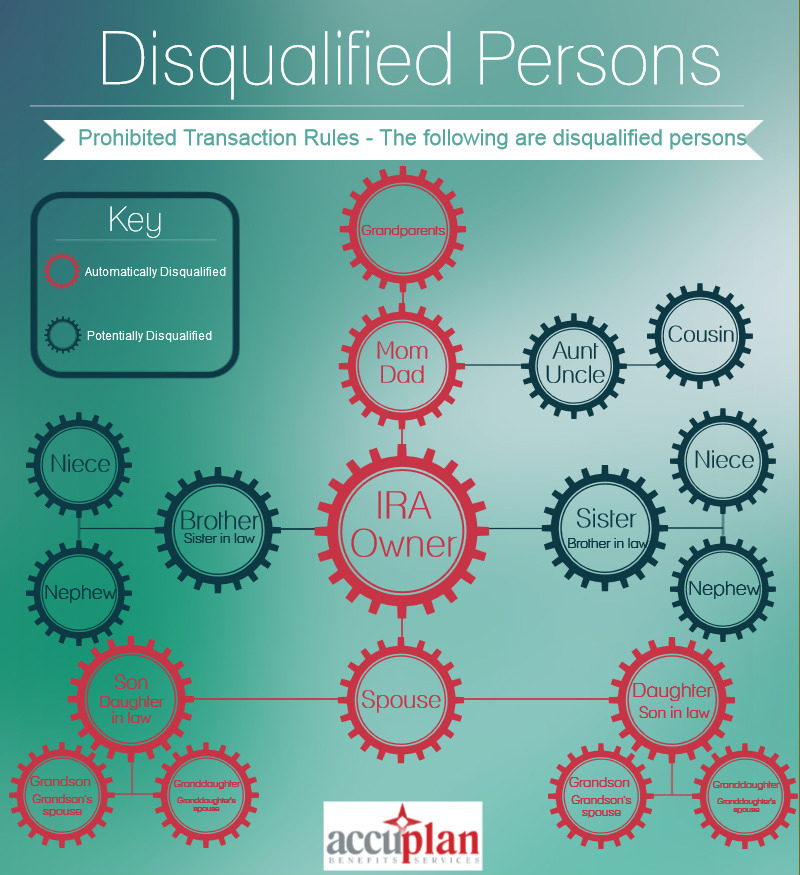

Examples of Disqualified Persons

You will be considered a disqualified person if you are any of the following:

- A fiduciary — or someone with a trusted relationship — to the plan.

- Direct family members, such as children, spouses, ancestors or other lineal descendants.

- Someone providing services to the plan.

- An employee or employer covered by the plan.

- A direct or indirect owner of profit shares in a company, partnership, trust or estate.

What Are Prohibited Transactions?

Prohibited transactions are transactions between the IRA and 401k plan that are not allowed by law. These scenarios include:

- A transfer of plan income to — or use for the benefit of — a disqualified person.

- The receipt of consideration by a fiduciary for their own account involving plan income or assets — usually for personal use.

- Using the plan as security for a loan.

- Selling, leasing or exchanging IRA-owned properties to related parties, as listed above.

- Furnishing services, goods or facilities to an investment property.

- Lending money or extending credit from accounts.

If you are considered a disqualified person and participate in any of these transactions, you will need to pay a tax of 15% of the amount involved for each year in a tax period. However, a disqualified person can avoid this tax if the prohibited transaction is corrected as soon as possible. This effort can include undoing most of the transaction without putting your plan in a worse financial position.

How Does a Prohibited Transaction Affect an IRA Account?

Suppose an IRA owner or any of their beneficiaries completes a prohibited transaction with an IRA account. The account will stop being an IRA on the first day of the year. The account will then be disqualified and treated as if it was fully liquidated in a taxable distribution. It is important to note that the whole retirement account will lose its tax-deferred status, not just the portion involved in the prohibited transaction.

Contact Accuplan Benefits Services Today

Understanding disqualified persons within an IRA or 401k account can be complex and challenging to take in at once. At Accuplan Benefits Services, our dedicated experts are passionate about helping you navigate all aspects of investing in a self-directed IRA. Our team will strive for professionalism and quality service in any situation you may face. Contact us today to get started!

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.