During immediate financial emergencies where other financial sources are challenging to leverage, hardship withdrawals from IRAs and 401(k)s can be a worthwhile option. Still, these have specific requirements you need to meet to leverage them without incurring a penalty or tax. This guide explores what qualifies for a hardship withdrawal, the process for approving it and additional financial planning strategies to help you cope financially during a hardship.

Penalty exceptions at a glance

The IRS waives the 10% early-withdrawal tax in specific situations. The list below covers every penalty exception that applies before age 59½. For the full criteria, see the IRS rules for IRA distributions and the IRS exceptions list for 401(k) distributions.

Available to both IRAs and 401(k)s

- Unreimbursed medical expenses above 7.5% of AGI. No dollar cap.

- Permanent and total disability. No dollar cap.

- Substantially equal periodic payments. No dollar cap.

- Qualified military reservist on active duty. No dollar cap.

- Birth or adoption of a child. Up to $5,000 per child, per parent.

- Federally declared disaster. Up to $22,000 per disaster.

- Death of the account holder. No dollar cap.

IRA only (not available from a 401(k))

- Health insurance premiums while unemployed. No dollar cap.

- Higher education expenses for self, spouse, or dependents. No dollar cap.

- First-time home purchase. Up to $10,000 lifetime.

SECURE 2.0 additions (automatic for IRAs; 401(k)s only if the plan adopts them)

- Emergency personal expense (2024+). Up to $1,000 per year.

- Domestic abuse victim (2024+). Lesser of $10,000 (indexed) or 50% of account.

- Terminal illness. No dollar cap.

- Long-term care insurance premiums (starts 2026). Lesser of $2,500 or 10% of account.

Two things to keep in mind. Standard income tax still applies to anything withdrawn from a pre-tax account, even when the 10% penalty is waived. Qualified Roth IRA distributions remain tax-free. And a 401(k) “hardship distribution” is a separate plan-level category. Your plan administrator decides what qualifies, and the 10% penalty still applies unless the reason also matches one of the exceptions above.

What Is a Hardship Withdrawal?

A hardship withdrawal is defined as an emergency withdrawal of retirement funds from a retirement plan. This type of distribution can be allowed without penalty from retirement savings vehicles like Traditional IRAs or 401(k)s, given that specific requirements are met. It’s important to note that even if all criteria are met on behalf of the plan’s owner, they still might incur standard income taxes.

What Qualifies for a Hardship Withdrawal From an IRA?

The Internal Revenue Service (IRS) created eligibility criteria for what qualifies as an immediate and heavy financial need or hardship. Here are the IRA hardship withdrawal rules about which financial hardships qualify for hardship withdrawals.

Medical

Within the IRA rules, there’s an IRS-mandated condition that a 10% penalty will be taken from the distributed funds if taken before age 59½. Suppose the IRA holder does not have health insurance or has medical expenses that are more than their insurance will cover for the year. In that case, they might be allowed to take penalty-free distributions from their IRA to cover these expenses. Note that only the cost difference between these expenses and 7.5% of the IRA owner’s adjusted gross income (AGI) is considered eligible.

Unemployment

If the IRA owner is unemployed, they’re permitted to take penalty-free distributions to pay for medical insurance premiums. To qualify, the IRA holder must have received unemployment compensation for 12 consecutive weeks. The distribution has to come in the year unemployment was received or the year after, and no later than 60 days after returning to work. There is no AGI threshold for this exception. See the IRS list of exceptions to the 10% additional tax for the full criteria.

Disability or Higher Education

The IRS allows for early, penalty-free withdrawals from IRAs for other reasons that may or may not be prompted by hardship. These include having a mental or physical disability or needing funds to pay higher education bills for the owner, spouse, children, or grandchildren.

Hardship Withdrawals From 401(k)

Whether or not one is eligible for an early distribution due to hardships or other reasons is entirely up to the 401(k) plan’s sponsor, either through employment or self-employment. The IRS states that “A retirement plan may, but is not required to, provide for hardship distributions.” It is solely up to the provider to specify the criteria that define a hardship. They may ask for information and documentation of said hardship.

If 401(k) plan withdrawals are permitted, the IRS governs whether the 10% penalty for withdrawals made before age 59½ will be waived, as well as how much can be withdrawn.

Medical insurance premiums cannot be made through 401(k) funds as they can with IRA funds. Withdrawals to pay for education or expenses for purchasing a first home (free of penalties) are not permitted within a 401(k) but are both allowed at a penalty-free rate for IRAs.

Process for Approving Hardship Withdrawals

Hardship withdrawals from an IRA or 401(k) require you to follow a five-step process to help ensure a smooth approval when you meet all the requirements. Here are the steps for submitting a hardship withdrawal application.

1. Have a Thorough Understanding of Which Hardships Qualify

First, you must understand whether the IRS might allow your hardship to qualify. The penalty exceptions section earlier in this guide lists every reason the 10% early-withdrawal tax can be waived, including the SECURE 2.0 additions for emergency personal expenses, domestic abuse victims, terminally ill account holders, and long-term care insurance premiums (effective 2026).

Available to both IRAs and 401(k)s:

- Birth or adoption of a child (up to $5,000 per child, per parent)

- Permanent and total disability

- Substantially equal periodic payments, per IRS SEPP guidance

- Federally declared disaster (up to $22,000 per disaster)

- Military reservists called to active duty

- Unreimbursed medical expenses above 7.5% of AGI

- SECURE 2.0 additions, where the plan permits them for 401(k)s: emergency personal expense ($1,000/year), domestic abuse, terminal illness, long-term care premiums (2026+)

Available to IRAs only (not 401(k)s):

- Health insurance premiums while unemployed

- Higher education expenses

- First-time home purchase (up to $10,000 lifetime)

2. Choose an Appropriate Amount Within the Limits

You may only withdraw as much as is needed for your financial hardship or up to a certain amount as defined by your plan. Before applying for a hardship withdrawal, carefully check how much you’ll be allowed to access according to IRS and plan rules without triggering additional taxes or a penalty. Based on this number, you may plan how you will use the money or if it may be necessary to consider alternative options.

3. Check Your Provider’s Eligibility Criteria

While you may qualify for a hardship withdrawal according to IRS rules, it’s equally important to check your plan provider’s criteria for hardship distributions. For example, your employer’s plan may include funeral and medical expenses as hardships reasons, while principal residence and education expenses are excluded. It’s also important to check whether you’ll still owe the 10% additional tax even if your plan classifies the request as a hardship distribution. The IRS waives that 10% only when the reason matches one of the penalty exceptions listed at the top of this guide.

4. Provide Proof of Your Hardship

According to the IRS, employers may allow employees to pursue a hardship withdrawal if they can demonstrate that they are experiencing an immediate and heavy financial need that may be challenging to relieve from other resources. These may include if they are unable to seek financial relief by liquidation of the employee’s assets, reimbursement or compensation by insurance, borrowing from commercial sources, stopping elective contributions or employee contributions under the plan or by using other currently available plan distributions maintained by the employer or another employer.

For this reason, it may help to submit relevant documentation, such as bills, invoices and legal documents, with your application to prove that you meet qualifications.

5. Submit the Request to Your Plan Administrator or IRA Custodian

The IRS does not pre-approve hardship withdrawal requests. For a 401(k), submit the request and supporting documents to your plan administrator, who applies the plan’s hardship criteria and processes the distribution if approved. For an IRA, the custodian processes the distribution without a hardship review, and the IRA holder self-certifies the reason for the penalty exception on Form 5329 when filing taxes.

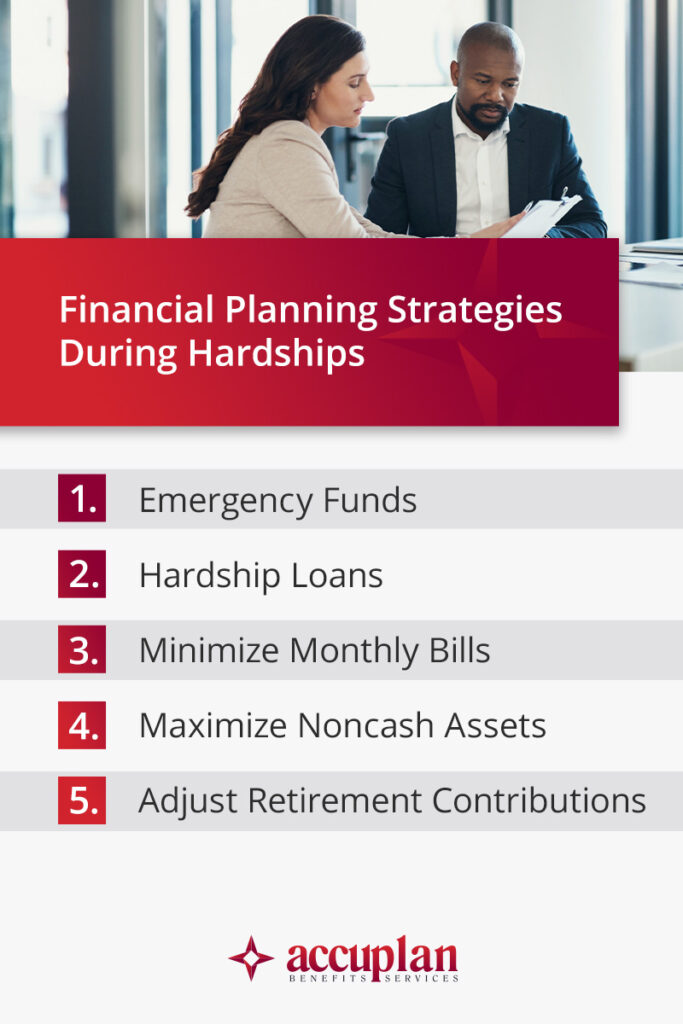

Financial Planning Strategies During Hardships

Whether you’re experiencing a hardship or creating plans for handling potential hardships in the future, it helps to consider different financial planning strategies to help you stay financially secure in addition to or without using a hardship withdrawal. Here are five strategies you could implement.

1. Emergency Funds

An emergency fund instead of a hardship distribution can be a better solution if financial emergencies or unplanned expenses come up. An emergency fund is typically a cash reserve built from monthly contributions in case an emergency occurs.

If you already have one, you may be able to use it instead of making a hardship withdrawal or in addition to your hardship withdrawal if your plan’s limit is less than the amount you need. If you have yet to build an emergency fund, you can create one by setting a savings goal and making consistent contributions.

2. Hardship Loans

Rather than doing a hardship withdrawal, you might opt for a hardship loan. While you cannot take a hardship loan from your IRA, you can take a loan from a 401(k).

A 401(k) loan may be an ideal option if your hardship does not cost much or if the hardship does not qualify as a heavy financial need to the IRS. If your plan sponsor allows loans, you may borrow $50,000 or 50% of your vested amount, whichever is lower. You have to pay interest, but that goes back into your retirement account, and you avoid paying taxes and penalties as you would with an early distribution.

Other alternative loans to try might include home equity loans or lines of credit for home-related hardships or other low-interest loan options for lower-cost hardships.

3. Minimize Monthly Bills

Review your recurring monthly expenses, subscriptions and services. You may find that you rarely use some purchases and subscriptions, like streaming apps. Try canceling these services to reduce your spending and switching to cheaper products and services for necessary monthly expenses. You may also cut back on expenses by avoiding unnecessary shopping and dining out and trimming utility bills.

4. Maximize Noncash Assets

Another helpful strategy involves taking stock of what you have around the house and maximizing its value. For example, if you have extra toiletry goods like soap, toothpaste and toilet paper for the month, you could create a plan to preserve them and skip buying them for the upcoming month. You may also lower your grocery bills by creating a meal plan to make your current food items last longer.

Lastly, you’ll want to check whether you have gift cards or unused items you could sell or use gift cards and credit card rewards for entertainment and meals.

5. Adjust Retirement Contributions

To reduce the money going out each month, you may want to lower your retirement contributions. This adjustment will allow you to reallocate some funds for a short period until your hardship becomes more manageable.

Learn About Your Hardship Withdrawal Options With Accuplan Benefits Services

IRA hardship withdrawals exist to help you through financially challenging situations. If you have explored all other options, our experts at Accuplan Benefits Services are available to help you understand IRS rules regarding hardship distributions from an IRA or 401(k). Our experienced team of professionals has vast industry knowledge of IRS rules and retirement accounts to provide personalized advice that allows you to follow the rules and avoid penalties. To learn more about your IRA hardship withdrawal options with Accuplan, contact our experienced team today.

Our information shouldn ’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.