Crypto IRAs have become a popular investment option for people looking to diversify their retirement portfolio with digital tokens such as Bitcoin, Ethereum and other cryptocurrencies.

Below, we will discuss self-directed IRAs for cryptocurrency and how you can start investing with Accuplan. Whether you are a seasoned crypto investor or just getting started, we will provide you with a comprehensive overview of this investment option and help you decide whether it is right for your portfolio.

What Is a Self-Directed IRA for Cryptocurrency?

A self-directed IRA for cryptocurrency is a retirement account that allows you to invest in virtual or digital tokens. Standard IRAs typically limit investments to stocks, bonds and mutual funds, while a self-directed IRA gives you more control over your retirement funds by allowing you to invest in alternative assets like real estate, precious metals and cryptocurrencies.

With a self-directed IRA for cryptocurrency, you can acquire and hold digital assets as part of a long-term investment strategy. These investments are stored securely in a digital wallet, providing the flexibility to trade them like any other investment. Additionally, the gains from the sale of cryptocurrencies held within a self-directed IRA are tax-deferred, enabling you to build wealth over time without immediate tax obligations until you make withdrawals.

However, self-directed IRAs for cryptocurrency come with some risks, including volatility and the potential for hacking or theft. If you choose to invest, it is crucial to do your due diligence and work with a reputable custodian to secure your retirement savings.

Overall, a self-directed IRA for cryptocurrency can be a valuable investment option if you want to diversify your retirement portfolio with digital assets. However, you must understand the risks and work with a trusted custodian like Accuplan to invest confidently.

Trade 120 Cryptocurrencies With Accuplan

Buying and selling crypto is effortless with Accuplan. Easily buy or sell your favorite coins from our crypto trading platform without ever having to leave the site!

We have simplified crypto buying and selling to make it approachable for anyone.

- Create an account: Start with our user-friendly application in only a few minutes.

- Fund your account: Transfer, roll over or contribute funds to your IRA account.

- Buy or sell crypto: Buy the coins you want right away. It’s that simple!

The future is here, and it’s time to leverage this technology to significantly enhance your earnings.

At Accuplan, we allow investors with IRAs or 401(k)s to access the potential profits of cryptocurrencies like Bitcoin.

Learn more about investing in crypto with an IRA from Accuplan.

Why Use Accuplan?

We have been doing nontraditional retirement investing for years. We have the knowledge needed to help you succeed with your retirement investing.

We know what investors are looking for and the support they expect. Take that knowledge and service and add a revolutionized crypto trading platform that allows you to invest, with or without your retirement account and you have a recipe for success.

Trading has never been simpler.

Trading transactions are fast with our crypto portal. All trades settle in under a minute, allowing for day trading of cryptocurrencies.

You won’t need to create a third-party trading account on another crypto-buying platform. Truly, this is all under one roof.

Is cryptocurrency right for your retirement?

Speak with the pros about investing in crypto today.

Frequently Asked Questions

Below are some frequently asked questions regarding Bitcoin IRAs.

There is a minor delay when you buy or sell Bitcoin. Because of this, the price you buy and sell at can be slightly different from the final buy or sale price.

Yes, you can purchase cryptocurrency 24 hours a day, seven days a week.

Below are the fees for a crypto IRA.

- Transaction fee: 1%

- Monthly storage fee: 0.05%

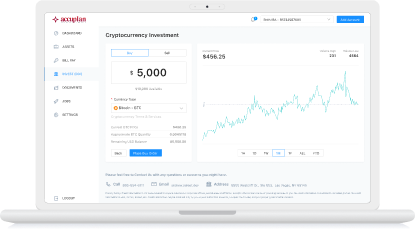

Follow the steps below to purchase crypto:

- Login or set up your account.

- Select “Invest (DOI)” on the far left.

- Select “New Investment” (blue button on the far right).

- Select “Cryptocurrency.”

- Agree to the terms and conditions.

- Enter the dollar amount you want to purchase.

- Select the cryptocurrency you want to purchase.

- Select “Place Buy Order.”

Follow the steps below to sell crypto:

- Login or set up your account.

- Select “Invest (DOI)” on the far left.

- Select “New Investment” (blue button on the far right).

- Select “Cryptocurrency.”

- Agree to the terms and conditions.

- Enter the dollar amount you want to sell.

- Select the cryptocurrency you want to sell.

- Select “Place Sell Order.”

We support all coins that are available through Coinbase. When you initiate the trade online, you can view all the coins offered. Currently, there are about 120.

Coinbase is the tool used to buy and store cryptocurrency.

You cannot hold your keys for security purposes to prevent hackers and impostors. American Estate & Trust has procedures through Coinbase that prevent direct coin removal. This high level of security prevents AET from transferring the assets themselves and prevents any hackers or impostors from initiating a transfer out.

You must place a sell order and then withdraw the funds in U.S. dollars. You cannot withdraw or move cryptocurrencies.

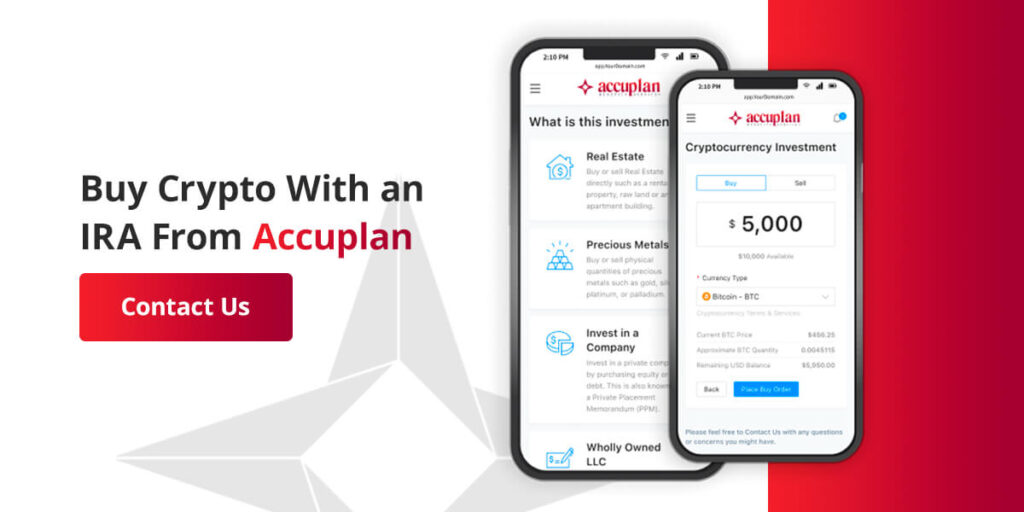

Buy Crypto With an IRA From Accuplan

When choosing a custodian for your self-directed cryptocurrency IRA, it is essential to consider factors such as fees, security measures, customer support and the range of assets that are available for investment.

At Accuplan, we specialize in providing custodial services for alternative assets, including cryptocurrencies, and offer a range of IRA options, including:

- Traditional IRAs

- Roth IRAs

- SEP IRAs

- SIMPLE IRAs

We also provide access to various digital assets, including Bitcoin, Ethereum, Litecoin and more. Additionally, we offer competitive fees, robust security measures and 24/7 customer support. We also provide educational resources and tools that can help you make informed decisions about your investments.

To get started and diversify your portfolio, open a self-directed IRA account for cryptocurrency with us at Accuplan today.

*Our information shouldn’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.