When choosing the best type of retirement account for your financial goals, you may want to minimize your tax obligations. Tax-deferred and tax-exempt accounts can help you retain more wealth over your lifetime. However, each of these retirement accounts handles taxes differently and has advantages at different times. Understanding the differences between these accounts helps you make the best decision for your retirement funds.

What Are Tax-Free vs. Tax-Deferred Accounts?

You will pay income taxes on your retirement funds one way or another. Tax-free accounts, also called tax-exempt accounts, are only tax-free on withdrawal and not when contributing, whereas tax-deferred accounts are the opposite.

However, strategically choosing where you place your assets and when you pay tax on them can reduce your lifetime tax burden. Tax-deferred and tax-exempt retirement accounts both offer tax benefits but receive different tax treatments, which may make one more appealing for your retirement savings.

Tax-Deferred Retirement Accounts Overview

The main difference in tax-exempt vs. tax-deferred retirement accounts is when the tax advantage applies. Tax-deferred retirement accounts provide an immediate tax benefit by deferring income taxes until you withdraw. Since money in a tax-deferred retirement account accumulates interest on pre-tax amounts, you benefit from tax-free contributions and pay taxes later.

Another significant difference between tax-deferred and tax-exempt retirement accounts is when owners can claim tax deductions for their contributions. Tax-deferred retirement accounts enable account holders to take tax deductions immediately, up to the total amount they’ve contributed to their accounts. However, you must pay income tax when you withdraw, so remember to factor this into your retirement plans.

The types of tax-deferred accounts include traditional IRAs and 401(k)s.

Traditional IRAs

A traditional individual retirement account (IRA) is a tax-deferred IRA that enables tax-deductible contributions. Features of traditional IRAs include:

- Pre-tax investments: Funds in a traditional IRA are only taxed when the account owner takes a withdrawal.

- Tax deductions: A traditional IRA enables fully or partially deductible contributions.

- Limited contributions: Tax-deferred IRA rules limit annual contributions, though people aged 50 and over have an additional “catch-up” limit on top of that. If someone participates in a workplace-sponsored retirement plan or makes above a specific amount, contributions to a traditional IRA may be limited.

- Minimum distributions: Traditional IRAs are also subject to required minimum distributions (RMDs) once the account owner turns 72. This means you must start withdrawing a minimum amount from your account at that time.

Most traditional IRAs are conventional, meaning a brokerage house manages the funds for the account owner. People who want more control over their traditional IRAs may prefer a self-directed IRA account.

Self-directed IRAs can be traditional or Roth accounts. These accounts function differently than conventional IRAs. Owners of self-directed IRAs direct their funds through a broker or account custodian and have greater flexibility when choosing their investments.

The same annual contribution limits apply to self-directed IRAs and conventional IRAs. However, self-directed IRAs allow you to invest in alternative assets like real estate, gold or private equity.

401(k)s

Another type of tax-deferred retirement account is the 401(k), which allows employees to contribute a portion of their wages to the account. Most 401(k)s are employer-sponsored retirement accounts, so account owners must go through their employer to make contributions. As with traditional IRAs, 401(k)s are subject to RMDs beginning when the account holder turns 72. However, they have higher contribution limits, allowing you to save funds more rapidly toward retirement.

Although most 401(k)s are employer-sponsored, self-employed people or those whose employer doesn’t provide the option can still open a self-directed 401(k) account. This type of 401(k) eliminates the employer’s role, giving the account owner more control over their investments.

Tax-Exempt Retirement Accounts Overview

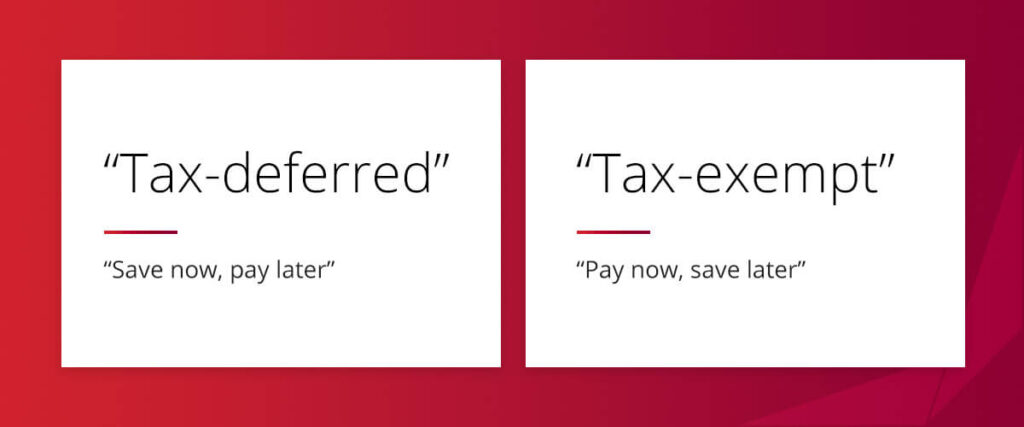

While both the major tax-deferred account types provide a tax break on contributions, tax-exempt accounts offer tax benefits upon withdrawal. Simply put, **tax-deferred means “save now, pay later,” and tax-exempt means “pay now, save later.” **

When you open a tax-exempt retirement account, they pay income taxes on their money before making contributions. Since tax-exempt retirement accounts use post-tax dollars, these accounts are entirely tax-free once you deposit the money. Although these accounts lack an immediate tax advantage, they allow income to grow without ever being taxed again.

The two types of tax-exempt retirement accounts are Roth IRAs and tax-exempt 401(k)s.

Roth IRAs

Roth IRAs are tax-exempt retirement accounts that allow you to make tax-free withdrawals upon retirement or other qualifying circumstances. Roth IRAs are subject to the same annual contribution limits as traditional IRAs. However, since Roth IRAs are not subject to RMDs, you can leave your money to grow as long as you like. Additionally, Roth IRA account owners must meet federal income limits to contribute and pay income tax on their contributions.

Roth IRAs may be conventional — where a brokerage house guides investments — or self-directed. Opening a self-directed Roth IRA account gives you more control over your investments and broader diversification.

Tax-Exempt 401(k)s

A Roth 401(k) is another retirement account you fund with after-tax dollars. This type of retirement account combines many features of those above:

- Qualified distributions are tax-free.

- There are no income limits for a Roth 401(k) account.

- Roth 401(k)s are no longer subject to RMDs for the original owner (eliminated in 2024 under SECURE 2.0).

- These 401(k)s have the same contribution limits as traditional 401(k)s.

- Self-directed Roth 401(k)s give account owners the flexibility to invest in real estate, precious metals, cryptocurrencies and more.

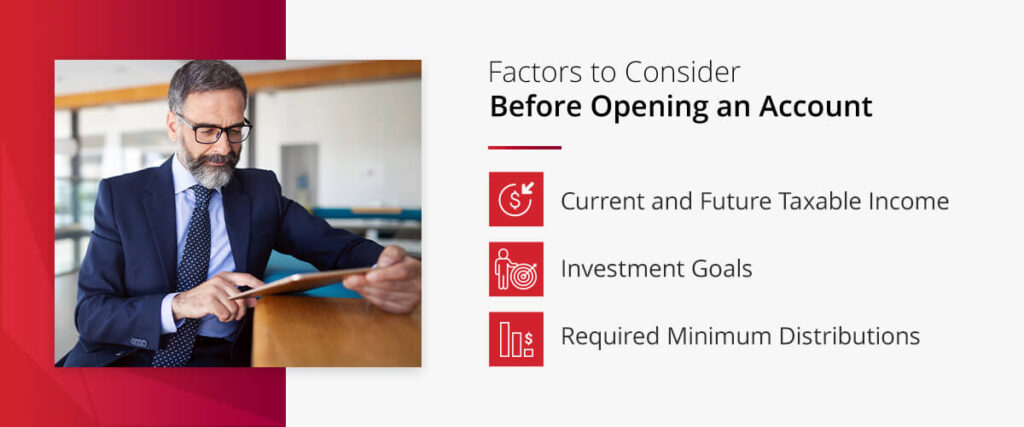

Factors to Consider Before Opening an Account

When comparing tax-deferred vs. tax-free accounts, consider your financial situation and goals. One account may help you maximize your wealth better than another, and some have limitations you may want to avoid. Consider the following factors before deciding which retirement account is best for you.

1. Current and Future Taxable Income

Many people enjoy the immediate tax benefit of a tax-deferred IRA or other tax-deferred retirement accounts. These accounts are often beneficial for high earners. A tax-deferred account minimizes taxable income, whereas a tax-exempt account requires you to pay the full income tax for your tax bracket. Because of those immediate tax savings, you may be able to afford larger contributions during your working years, boosting your retirement savings progress. However, if your income is low right now, you may save more by paying taxes upfront and withdrawing tax-free when you retire.

Future taxable income is another crucial consideration. Since many people have a lower taxable income after they retire, paying taxes on withdrawals during retirement and reducing their taxable income now may minimize their tax burden. If you expect your income to increase over time, it may be wiser to choose a tax-exempt account so you can pay taxes while in a lower bracket and benefit from tax-free withdrawals later.

2. Investment Goals

Some investors like holding assets for long-term growth, while others are more active and prefer an aggressive approach. Keeping your investment goals in mind is essential when selecting a retirement account. Tax-exempt accounts may appeal more to aggressive investors because they can realize tax-free capital gains when selling assets.

Self-directed retirement accounts are ideal for active investors. These accounts give you more control over your investments and allow for a broader portfolio.

Whether you opt for a more conservative or aggressive investment strategy depends on your time horizon and preferences. In general, investors closer to retirement enjoy the security of a buy-and-hold approach, while those starting early have the risk tolerance to pursue higher returns with more aggressive strategies.

However, you may be an exception, depending on your temperament and circumstances. A self-directed account lets you take charge of your investment strategy, adapt to changing circumstances and diversify across asset classes to protect your funds.

3. Required Minimum Distributions

RMDs may be another factor to consider when deciding on a retirement plan. While owners of traditional IRAs, 401(k)s and Roth 401(k)s must begin taking distributions at 72, Roth IRA account owners can leave their investments to grow throughout their lives. This means you can save your entire Roth IRA for your family to inherit if you have enough retirement funds in your other accounts to cover your needs.

Although traditional IRAs and 401(k)s have RMDs from age 73, you can withdraw without penalties from age 59 ½, and you may withdraw more than the minimum.

Open a Tax-Deferred or Tax-Exempt Account Today

Tax planning is crucial for your retirement and investment decisions. A tax-deferred or tax-exempt retirement account may help you achieve your financial goals.

If you want to invest your retirement funds in alternative assets like real estate, precious metals and cryptocurrencies, a bank or brokerage firm may not give you the options you want. At Accuplan, we offer self-directed tax-deferred and tax-exempt retirement plans to expand your investment opportunities. With a self-directed retirement plan, you can invest in what you’re passionate about.

Our team at Accuplan has vast industry experience and knowledge to help you fund your retirement, your way. Create an account or contact us today to get started.

Our information should not be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied on for, legal, accounting, investment or tax advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.