The enduring popularity of the F.I.R.E. (Financial Independence, Retire Early) movement has revealed an intense interest in the idea of early retirement. There’s no doubt that the desire to retire years or even decades before passing the 60-years-old mark is alive and well in the 21st century.

While retiring young is a hot topic, it does raise the question: is it worth it? Once you have your individual retirement account set up and you’ve maximized your contributions, lowered your expenses, set up an emergency fund and generally prepared for the unexpected, is it a good idea to permanently tap out of the professional workforce?

If you’re considering retiring before 50, here are a few of the most important pros and cons to consider.

Pros of Retiring Before 50

Many alluring factors come with early retirement, though which is most appealing depends on your goals, profession and even your expectations for retirement. How much free time is available also depends on what specific steps you’ve taken to retire early, and whether you plan to leave the workforce entirely. Here are the advantages of taking an early retirement.

Travel Opportunities

It’s difficult to travel much when you only have a handful of vacation days each year. Once you’re retired, you’re able to largely do as you please with your time — including traveling. Many people hope to travel during retirement and visit destinations across the U.S., Europe and beyond. Early retirement is an excellent opportunity to go on sightseeing tours, adventurous vacations or relaxing trips, allowing you to tick off locations on your bucket list one at a time. For more extensive or physically challenging travel plans, like outdoor adventures or long flights, it’s often better to travel as a younger person when retiring at an early age.

Taking on New Hobbies or Volunteering

The intense demands of a full-time job leave little room for extracurricular activities. Most of the time your interests must take a backseat to the need to either work or rest and recuperate.

Once you’re retired, though, the dramatic uptick in free time can be filled with a variety of activities that were previously difficult to prioritize. Items of particular note for many include:

- Cultivating new interests: You’ll have plenty of time to identify and pursue new interests and curiosities that may have never caught your attention beforehand.

- Developing hobbies: Both old and new hobbies can be fostered during retirement.

- Volunteering: Giving your time and effort to causes that you care about is always fulfilling — and when you’re retired it’s much easier to do so.

From personal interests to helping the community, there are many positive and rewarding ways to fill up your retired lifestyle. Another advantage of taking up new hobbies when retiring before your 50s is that you have more energy than if you retired later. Extra energy and stamina allows you to fully enjoy the experience and potentially even monetize certain hobbies so you continue to earn money in retirement.

Time to Spend With Family and Friends

When you’re working full-time, one of the primary goals is to facilitate a comfortable life for you and your family. Unfortunately, one of the trade-offs of this arrangement is the fact that you also spend most of your time at work or in your home office.

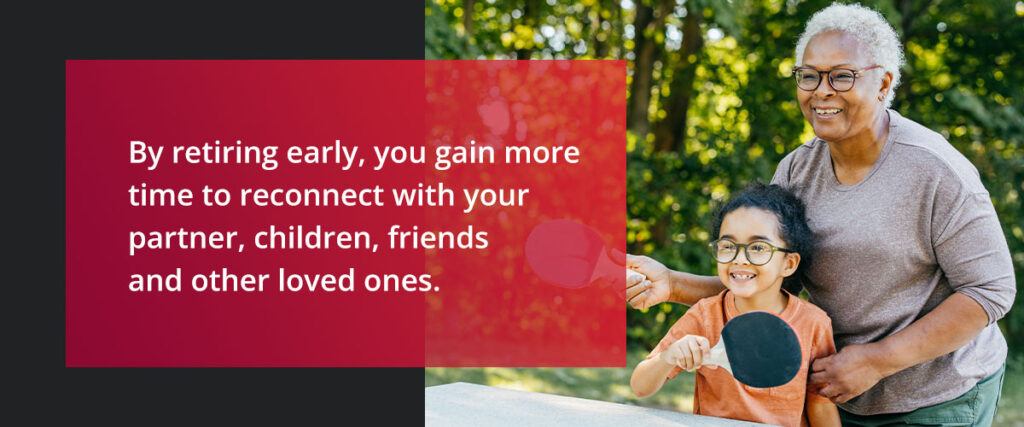

Once you’re retired, this is naturally resolved by your financially stable life and open schedule. You can plan as much time with your friends and family as you please. Many retirees view this as the biggest benefit of an early retirement. By retiring early, you gain more time to reconnect with your partner, children, friends and other loved ones. This is also a great opportunity to actively engage in your children’s lives.

Your Health

When you’re younger, it’s tempting to ignore physical health concerns as you focus on things like earning an income or caring for your dependents. However, retiring early allows you to take the time to put your health first.

This doesn’t just refer to going to a yearly physical checkup or finally booking an appointment with the dentist, either. It also means you can address multiple easily overlooked areas of health management, including:

- Your lifestyle: Retirees can take the time to correct unhealthy habits like staying up late or eating fast food on the way to work.

- Your living environment: If you live in an area where the weather or your current housing is unhealthy, retirement provides the freedom to address the issue.

- Cultural norms: Things like pressure to spend all of your time at the office or a lack of spare time for physical activity.

While it takes some preparation and commitment, living an early retired life can have some genuinely wonderful perks.

Cons of Retiring Before 50

Every coin has two sides, and these are a handful of the biggest concerns that come with retiring early.

Money Can Be Tight

The most obvious struggle of early retirement is ensuring that you have the money to go the distance.

For instance, you don’t know how long you’ll live. At 45 or 50 years old, you may only be halfway through your life and all of the expenses related to it. You also can’t predict how the cost of living will change or if your retirement fund will suffer through economic hardships down the road. This means you may have to ensure your savings last decades longer than you initially planned.

It’s also important to consider if and when you’ll be able to withdraw from a 401(k) or IRA without penalties from the IRS. Even when you do so, will you need to pay income tax on the money? Are you missing out on years of potential growth necessary to build your saved cash into a bona fide nest egg? These are the kinds of questions that must be answered before you commit to the retired lifestyle.

Health Care Costs

No matter how healthy you are, sooner or later significant medical bills are probably going to creep into the picture.

When this happens, will you have the financial stamina to pay them? Even if you do so, will it be at the cost of compromising on your retired lifestyle? Health care costs are a genuine concern that, unfortunately, cannot be predicted. At the same time, you may only qualify for Medicare once you reach age 65 — before then, you may need to make a way to pay health care costs on your own during retirement.

Social Security Benefits May Shrink

Before taking an early retirement, it’s essential to consider your retirement income, savings and investment portfolio. Along with having to wait that much longer for your Social Security benefits, it’s also important to remember that those benefits may be lower once you get them. Why? Well, if you feel a financial pinch in the decade or more before you reach the normal retirement age of 67, you may be tempted to cash in on your benefits as soon as possible.

The earliest that you can collect these benefits is at the age of 62. However, if you do so, you’ll end up getting roughly 30% less in each payment than if you waited until you were 67. Also, if you defer collecting payments from 67 to 70, the payment increases by an additional 8% each year.

All that to say, if you end up taking Social Security sooner, you’ll pay for it in the long run.

Difficulty Paying Off Debt and Loans

Another concern that works against early retirement benefits is you may need to factor in unpaid loans and debt to pay off during your early retirement. This may strain you financially, making it essential to either find ways to close all loans before retirement, or create a repayment strategy to implement into your retirement financial plan. It’s also important to keep in mind that interest rates may rise, so it’s a good idea to factor in buffers for any potential increases.

Mental Health and Overall Wellness May Suffer

If you opt to retire as soon as possible in the name of doing nothing, there’s a chance that you’ll find yourself bored or feeling lonely. There’s even clinical evidence that for some people, retirement can lead to a decline in physical and mental health, while other retirees report an overall improvement in mental health. It is important to be self-aware and have a plan to practice self-care in retirement.

The way that you live life and the kind of personality that you have should heavily factor into the equation. If you’re a go-getter, do you have activities and interests that you can pour yourself into once you’re out of the workforce?

Fortunately, if you do choose to retire early and find it isn’t something you enjoy, it doesn’t mean you’re stuck. While there are some possible financial repercussions, it’s certainly an option to come out of retirement further down the road.

Prepare for Your Retirement With Accuplan

Should you retire early if you can afford it? As long as you have the right retirement accounts and investment strategies, retiring before your 50s may be an option. It’s important to consider the early retirement benefits and drawbacks, and work with a team of financial experts like Accuplan.

Accuplan provides self-directed retirement accounts like an IRA and 401(k). With a self-directed retirement plan, you can build savings and use it to invest in conventional assets like stocks and bonds, and other asset classes such as real estate properties. Our team will guide you through the process of personalizing your investment strategies and ensure your account remains compliant.

Whether you want to learn more about early retirement or start saving for retirement at any age, contact us today or open a retirement account with Accuplan to get started.

Our information shouldn’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.