One of the biggest challenges of finding a mortgage lender and buying real estate is saving enough money for the down payment. In some cases, you might find it beneficial to use your self-directed 401(k) to complete the purchase. Like any financing option, buying a property with your 401(k) comes with various pros and cons. In this guide, we’ll explore everything you need to know, including the types of real estate you can buy, different ways you can make the purchase, and the benefits and drawbacks of using a 401(k) for financing.

Can I Use a 401(k) to Buy Real Estate?

Yes, you can use your 401(k) to buy real estate. Investors can purchase a house or land with 401(k) funds as long as they abide by the IRS’s rules and regulations. For the full step-by-step process, see our complete Real Estate IRA guide.

Even so, it is recommended to use 401(k) funds after retirement. Withdrawing funds from a 401(k) before you are 59 ½ will result in a 10% early withdrawal penalty and additional taxes. In other cases, you need to be at least 55 to negate taxation and penalties if you have lost or left your job.

Types of Real Estate You Can Buy With Your 401(k)

You can use your 401(k) to buy many types of properties. Check with your plan administrator for more specific information about what you can purchase, since the types of eligible real estate may vary based on your particular plan.

For example, there may be rules that make you unable to use your 401(k) to submit a down payment for your primary residence or to buy the house you live in. In other situations, you may only be allowed to use your 401(k) for rental property or other investments.

Here are six types of real estate you may have the option to purchase:

- Residential real estate

- Commercial real estate

- Mortgage notes

- Real estate investment trusts

- Tax liens

- Hard money loans to real estate developers

How to Buy a House With a 401(k) Plan

There are two options for using your solo 401(k) to buy real estate — borrowing funds from your 401(k) as a loan or making a withdrawal from your 401(k) account.

Get a 401(k) Loan

With a 401(k) loan, you can avoid the 10% early withdrawal penalty and additional taxes on the amount you withdraw. This type of loan allows you to withdraw a maximum of 50% of your 401(k) balance or up to $50,000. You will likely need to repay this amount with interest.

Make a 401(k) Withdrawal

A 401(k) withdrawal, also called a hardship withdrawal, is a desirable option if you are experiencing a heavy financial need. To qualify, you must provide your employer with proof of hardship, and the employer will decide whether it is an immediate need. However, this option will incur a 10% early withdrawal penalty.

Benefits of Using a Self-Directed 401(k) to Buy Real Estate

Using your 401(k) funds to buy a property can have many advantages. These perks depend on whether you choose to take out a 401(k) loan or a 401(k) early withdrawal.

Here are the benefits of using a self-directed 401(k) loan for real estate purchases:

- Avoid credit checks: 401(k) loans won’t appear as existing debt on your credit report, meaning it won’t impact your credit score in any way.

- Negate penalties and taxes: Borrowing from a 401(k) account allows you to avoid early withdrawal penalties and taxation.

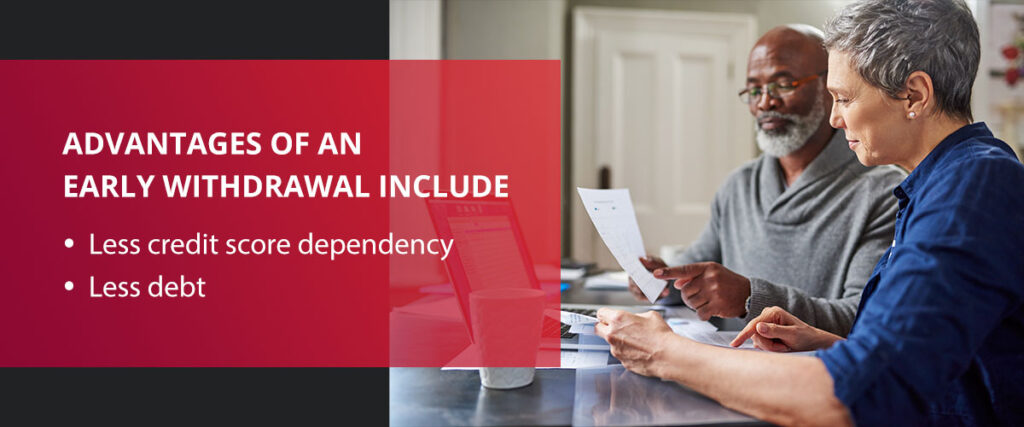

Advantages of an early withdrawal include:

- Less credit score dependency: Early withdrawals have less dependency on your credit score, making it easier to secure money for real estate and rebuild credit.

- Less debt: An early withdrawal gives you the financial flexibility to buy real estate and avoid paying back funds as you would have with a mortgage and 401(k) loan.

Drawbacks of Buying Real Estate With a Self-Directed 401(k)

While there are advantages to using a self-directed 401(k) to buy real estate, this method also has significant drawbacks to take note of when securing funding for land or a home.

The cons of using a 401(k) loan include:

- Failure to repay results in extra costs: If you find it challenging to repay the amount, the IRS may consider changing the loan to a hardship withdrawal and charge you a 10% penalty and any taxes on the amount borrowed.

- Employer will pause contributions: Your employer may stop contributing to your 401(k) plan until you pay back the entire amount of the loan, potentially altering your retirement plan and making a significant financial impact. With this in mind, the 401(k) loan may make sense only if you can handle the financial impact.

Drawbacks of a withdrawal include:

- You may lose 10% of the withdrawal amount: Unless you qualify for an exemption, the IRS will request a 10% early withdrawal penalty, which is money you would have received if you withdrew post-retirement.

- Potential to lose more money than you gain: With an early withdrawal, the IRS will charge you for taxes, making you lose more money from your 401(k) account than you would have gained in cash. This fact makes it essential to calculate the costs beforehand to see if you can afford to lose this money.

Tips for Using Your 401(k) to Purchase Real Estate

Are you unsure if using your 401(k) to purchase real estate is the best option? Fortunately, there are alternatives you can consider, including:

- Delaying your purchase: If you can delay the purchase of a property, you can both save up for a down payment and continue contributing to your 401(k). This may put you in a better financial position than if you were to use your 401(k) to buy real estate now.

- Exploring FHA loans: The Federal Housing Administration (FHA) offers loans to first-time homebuyers if they meet certain criteria. This option may allow you to make a lower down payment.

- Using an IRA: An individual retirement account (IRA) is an excellent option for buying real estate if you need to withdraw $10,000 or less, and it comes without any penalties attached.

Use Your 401(k) to Buy a Home or Land With Accuplan

Using your self-directed 401(k) to purchase real estate is a big decision to make. That’s why it’s important to know all your options and what to expect along the way.

With Accuplan, you can start investing in a wider range of assets and take control of your retirement savings. Our experts specialize in self-directed retirement accounts like 401(k) and IRA. We also offer administrative support, such as tax reporting and record-keeping for your 401(k) plan. Whether you need expert advice or want to open a self-directed retirement account, contact us today to learn more.

Our information shouldn’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.