A Savings Incentive Match Plan for Employees (SIMPLE) IRA is an individual retirement account set up for employees through smaller employers. Typically, these smaller employers have a maximum of 100 employees and do not offer any other retirement plan.

If you are a small business owner looking for employee retirement plan options, you may be considering a SIMPLE IRA. A SIMPLE IRA can be an ideal start-up retirement savings plan if you are a small employer and are not currently sponsoring another retirement plan for your employees. This retirement plan can offer several benefits for you and your employees.

4 SIMPLE IRA Basics Small Business Owners Need to Know

To determine whether a SIMPLE IRA plan is right for your small business and employees, consider the basics of this type of retirement plan:

1. Can a New Employee Contribute to a SIMPLE IRA?

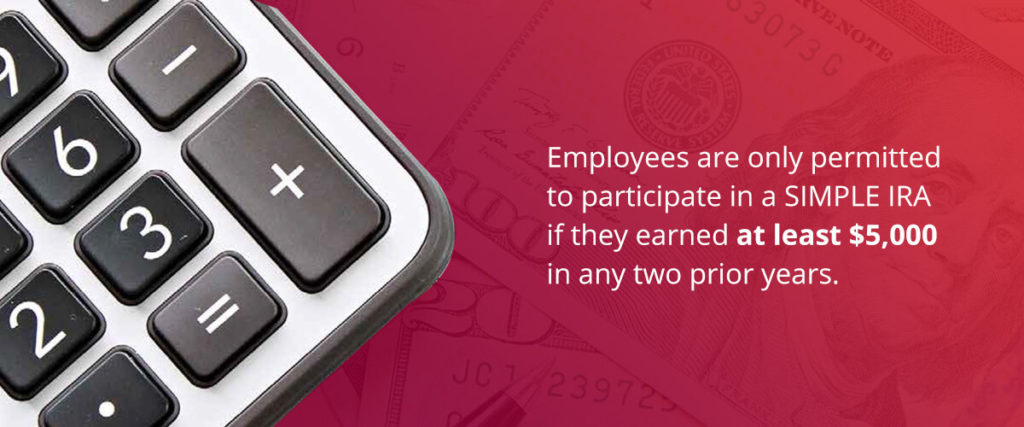

A new employee may not be eligible to contribute to a SIMPLE IRA. Employees are only permitted to participate in a SIMPLE IRA if they earned at least $5,000 in any two prior years. Employees who have just started working for your small business may not be eligible to contribute.

2. SIMPLE IRA Employee Eligibility

The IRS has distinct rules that an account owner must follow to remain eligible. Eligibility requirements for employees include:

- The employee expects to earn a minimum of $5,000 in the current calendar year.

- The employee must work for a small employer with no more than 100 employees or be self-employed.

- The employee must have earned a minimum of $5,000 during any two years before the current calendar year.

3. Advantages of a SIMPLE IRA

The benefits of a SIMPLE IRA include the following:

- Tax-deductible contributions: As an employer, you may receive a tax deduction for the contributions you make to your employees’ SIMPLE IRA plans.

- Minimal paperwork requirements: Another one of the advantages of a SIMPLE IRA is that they require minimal paperwork. The only required paperwork includes annual disclosures to employees and an initial plan document.

- Low setup and management costs: SIMPLE IRAs are widely used by small business owners because of their low setup and management costs.

4. How to Open a SIMPLE IRA

Follow the steps below to establish a SIMPLE IRA for your employees:

- Learn more about the self-directed accounts that we offer.

- Open an account with us at Accuplan.

- File Form 5305-SIMPLE to select the type of plan.

- Give eligible employees information regarding the plan.

- Use Form 5305-SA or Form 5305-S to set up separate plans for your eligible employees.

Contact Us for the Best SIMPLE IRA for Small Businesses

At Accuplan, we provide self-directed IRA administration. We have played an integral role in the success of thousands of investors. Our dedicated experts have years of experience in the retirement account industry and can help guide you through opening and investing in a SIMPLE IRA. Contact us at Accuplan to learn more about a SIMPLE IRA for small business owners, or open an account with us today.

*Our information shouldn ’t be relied upon for investment advice but for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.