You can save for a comfortable retirement by contributing to your 401(k) or IRA throughout your working life. The goal is to keep as much of your savings as possible when you reach retirement age. However, if you don’t take your required minimum distributions (RMDs), you may lose some of that money you’ve worked to save.

What Are Required Minimum Distributions?

An RMD refers to how much money you must withdraw from your retirement account when you reach retirement age. As the name suggests, RMDs only dictate the minimum amount you must withdraw, but you can withdraw more than that amount.

RMDs apply to various retirement accounts, such as:

- SEP IRAs

- 401(k) plans

- SIMPLE IRAs

- 403(b) plans

- Traditional IRAs

- Profit sharing plans

While RMDS only begin for Roth IRAs after the account owner’s death, the RMD rules do apply to the beneficiaries.

What Is RMD for IRAs?

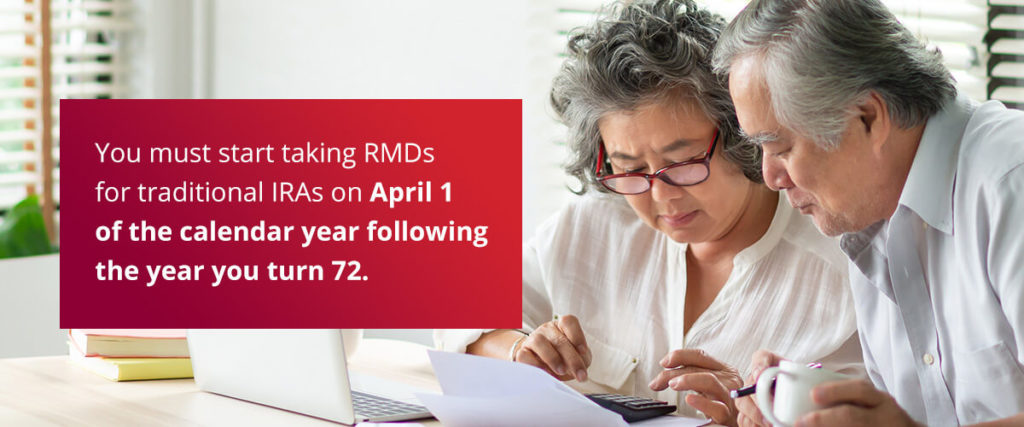

You must start taking RMDs for traditional IRAs on April 1 of the calendar year following the year you turn 73. For example, if you turn 73 in 2026, you would need to start taking RMDs on April 1, 2027. This rule applies to SIMPLE and SEP IRAs. (Note: the RMD age rises to 75 starting in 2033 under SECURE 2.0.)

How Do I Calculate My Required Minimum Distribution?

Your account custodian may be able to let you know the RMD for your account. You can also calculate your RMD by using the most up-to-date calculation worksheets from the IRS. Different calculation tables apply to different situations, and the IRS updates the tables with adjustments in life expectancy. If you hold a traditional IRA account, you can calculate your RMD by following the steps below:

- Note your account balance at the end of the previous year.

- Review the IRS calculation tables to identify the distribution factor corresponding to the age you will turn this year.

- Divide your account balance by the distribution factor to calculate your RMD.

How Are Required Minimum Distributions Taxed?

Withdrawals from many types of retirement accounts will be taxable. Exceptions include previously taxed contributions or funds you can withdraw tax-free, like qualified distributions from a Roth IRA account. For example, you may not need to pay taxes on your withdrawal if your RMD is from a Roth 401(k).

RMDs from 401(k) and traditional IRAs typically require you to pay taxes. If you do not take your RMDs or if your RMDs are not large enough, the IRS may charge you a 25% excise tax on the amount that was not distributed as required. If you correct the shortfall within two years, the penalty drops to 10%. File IRS Form 5329 to report the excise tax.

Contact Us at Accuplan

At Accuplan, our mission is to empower you as an investor and help you grow your retirement funds. Choose a self-directed IRA to invest in alternative assets like precious metals and real estate. Contact us at Accuplan to learn more about RMDs or open an account with us today.

Our content should not be relied on for investment advice but simply for informational or educational purposes only. Our information is not meant to provide, nor should it be depended on for advice regarding investment, tax, legal or accounting concerns.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.