Self-directed IRAs (SDIRAs) offer investors the opportunity to take more control over their retirement savings by investing in a wider variety of assets beyond traditional mutual funds, stocks and bonds.

With a self-directed IRA, you can invest in alternative assets such as real estate, private equity and precious metals. However, a self-directed IRA comes with its own set of rules and regulations that investors should be aware of before diving in.

We cover the basics of self-directed IRAs, their benefits and risks and how you can open one below.

What Is a Self-Directed IRA?

A self-directed IRA is an individual retirement account that, unlike traditional options, empowers the account holder to steer their retirement funds into alternative assets, thereby expanding investment portfolio options beyond standard choices.

On the other hand, standard IRAs held at brokerage firms or banks limit available assets to more conventional categories, such as stocks, bonds, and mutual funds.

Additionally, an Accuplan self-directed IRA account is an alternative asset IRA that has the power to invest in a wide range of available assets, unlike those standard investment accounts. Popular options include rental properties, loans and cryptocurrency.

Opening Your Own Self-Directed IRA Account

We have made our application process simple for client convenience. Specifically, all that’s required to get started is the account holder’s personal information and funding information from an established IRA or a brand-new retirement savings account.

Personal information you will need:

- Social Security Number

- Date of birth

- Contact information: phone number, email address

- Mailing address

- Image of your valid photo ID

To fund your account, options are:

- Direct contributions, for 2024 the annual contribution limit is $7,000.

- Rollover an established IRA, 401K, or another type of tax-qualified account

- Transferring funds or assets from one provider to another within the same retirement account type

Investing has never been easier:

To invest your IRA funds, you will fill out a direction of investment(DOI) form, found on your account dashboard. From there you can easily self-direct your tax-advantaged funds.

Call us at 800-454-2649 for assistance.

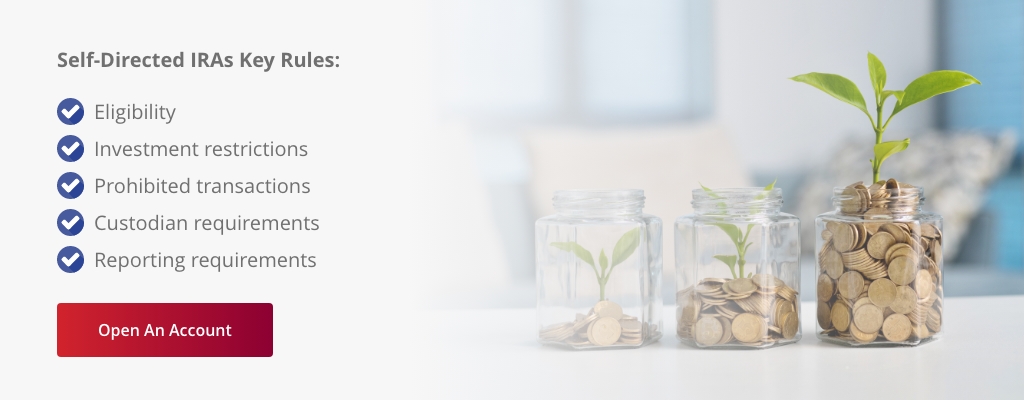

Self-Directed IRA Rules

When operating a self-directed account, it is imperative to follow all IRS rules and laws or the IRA could be subject to fines and penalties. Commonly broken self-directed IRA rules are prohibited transactions and investments, indirect benefits, disqualified persons and contribution limits.

Self-directed IRAs are subject to the same rules as traditional IRAs and Roth IRAs, as well as some additional rules and restrictions. Here are some key self-directed IRA guidelines to keep in mind:

- Eligibility: To contribute to a self-directed IRA, you must have earned income and be under a certain age.

- Investment restrictions: While self-directed IRAs allow for a wide range of alternative investments, there are still restrictions on certain investments. For example, you cannot invest in life insurance contracts or certain types of precious metals.

- Prohibited transactions: Self-directed IRAs are subject to strict rules regarding prohibited transactions, which can result in severe penalties and taxes. For example, prohibited transactions include utilizing IRA funds to purchase personal property, loaning IRA funds to yourself or family members, and purchasing assets from yourself or family members.

- Custodian requirements: Self-directed IRAs require a custodian to hold and manage the assets. The custodian must be a qualified financial institution that is approved to serve as a custodian for self-directed IRAs.

- Reporting requirements: Self-directed IRA holders are required to report all contributions and distributions on their tax returns. In addition, the custodian must report any transactions or holdings within the account to the IRS.

Most Common Alternative Assets

There is a wide range of alternative assets that can be held in a self-directed IRA, including:

- Real estate: This is one of the most popular alternative assets for self-directed IRAs. You can use your IRA funds to purchase rental properties, vacation homes and other real estate investments.

- Private equity: Private equity investments, such as venture capital and angel investing, can also be held in a self-directed IRA.

- Precious metals: Self-directed IRAs can invest in precious metals, such as gold and silver, either in physical form or through exchange-traded funds.

- Cryptocurrencies: Some self-directed IRA custodians allow for investment in cryptocurrencies.

- Private debt: Self-directed IRAs can invest in private debt opportunities, such as promissory notes and private loans.

- Private placements: Private placements, which are securities offerings that are not publicly traded, can also be held in a self-directed IRA.

Do Even More With an IRA LLC

Control when and where you direct retirement funds. An IRA LLC can offer the following benefits:

- Gain protection on assets within the LLC control: As the owner of the IRA LLC, you receive a physical checkbook that’s tied to your IRA funds so you can direct retirement investments. This means there’s no need to wait around for the custodian to approve and control your funds. You can do it yourself. In fact, an IRA LLC is a popular tool for real estate investors, who often need quick access to cash to pay vendors, repairs, and fees associated with property management.

- Asset protection: An IRA LLC acts like a corporation because it provides the owner with limited liability. The actions and the debts of the IRA LLC are held within the LLC, so losses, issues or other mishaps are contained to the LLC, protecting you and the asset.

How Accuplan Helps You Put Your Plan into Action

At Accuplan, we help you put your plan for investing into action.

Investing Your Way

Accuplan offers a genuinely self-directed IRA that allows for the complete customization of a retirement portfolio. On top of our SDIRA services, we also house HSAs, Employee Wellness Programs, LLC creation, 401K and business accounts, and everything required to operate a retirement account successfully.

Decades of Leadership

Since 2007, our dedicated team has been working hard for our clients. We have constantly been innovating, and we are invested in our clients.

Continuing Education

Our goal is to educate our clients on all IRS laws, rules continuously, and any new SDIRA updates that impact their retirement plans. Therefore, we provide quarterly educational newsletters, weekly blogs, educational videos, and asset guides.

Intuitive Dashboard

Our alternative investment platform is built for investors by investors.

What Accuplan Customers Are Saying

“Ben Barker is the most helpful person. He has saved me on several occasions. He probably saved me from paying over $50,000 in personal income taxes. I have been Ben’s customer for almost four years, and every time I call him or need advice, he has been there. Ben also personally set up my self-directed IRA LLC so I can manage my real estate holdings. Ben is an incredible and knowledgeable resource at Accuplan. Thanks again, Ben. I could not have done this without you. “

-Captain Chris Liu, San Francisco, CA

Self-Directed IRA FAQs

Below are some of the frequently asked questions we receive regarding self-directed IRAs.

Yes. Accuplan’s clients have complete access to invest in all types of real estate, like rental homes, commercial real estate and raw land. The investment options are limitless so long as you are following the IRS guidelines.

Unrelated Business Income Tax (UBIT) refers to the taxes that the IRS can charge based on a tax-exempt asset. Unrelated Business Taxable Income (UBTI) is the type of income that is taxable. And Unrelated Debt-Financed Income (UDFI) is used on assets that generate income that’s debt-financed like real estate.

The contribution limits for a self-directed IRA are the same as traditional and Roth IRAs. Currently, the maximum contribution limit is $7,000, with an additional catch-up contribution of $1,000 for individuals who are 50 years old or older.

Contribution limits may be subject to income limitations and eligibility requirements. For example, if you have a traditional IRA and participate in a workplace retirement plan, such as a 401(k), your ability to deduct contributions to your traditional IRA may be reduced or eliminated depending on your income level.

It’s always a good idea to consult with a financial advisor to ensure that you are following the contribution limits and guidelines for your specific situation.

We have a flat, non-percentage-based fee structure, so no matter how much your account grows, an annual fee will remain a flat $349.95.

We simplified our application process for self-directed IRA setup, so it only takes you minutes to get started. Follow these three easy steps to open a self-directed IRA account:

- Fill out the application.

- Fund your account.

- Direct your funds.

Look for an account custodian that is reliable, affordable and experienced in the industry. Accuplan Benefits Services has been an industry leader for decades. Invaluable experience and expertise come standard. Our fees are among the lowest around. We offer a flat, non-percentage-based fee schedule, so your fees never grow, but your IRA funds will.

Being able to rely on Accuplan as your administrator is imperative to your success. Our team is dedicated to serving you, answering questions, keeping your account IRS-compliant and assisting in any way that we can.

Some key self-directed IRA benefits include tax-deferred or tax-free profits, investment diversity allowing for a range of asset investments, and the potential to build wealth for future beneficiaries.

Your IRA cannot invest with the following related parties:

- Direct lineal family members. Linear family members include parents, grandparents, children, and grandchildren.

- A fiduciary of the IRA.

- Any person who has authority or control over your IRA or provides fee-based investment advice.

- Any person who has discretionary authority to administer your IRA.

Self-directed IRAs are self-managed in that you will be finding and choosing the investment and doing any due diligence that goes along with investing. Choosing your assets can be daunting to some and puts pressure on the individual account owner. As always, Accuplan is here to help guide and keep you in line with rules and regulations.

An IRA custodian is required to file Form 5498 both to the client and to the IRS. Distributions made throughout the year would require the custodian to report Form 1099 to the client and the IRS.

Typically no reporting is needed from the client as long as no distributions have been made and the client is not required to take distributions due to age. If the client has distribution requirements, has an IRA LLC, or has received debt financing inside the IRA, they may be required to report filings to the IRS.

We recommend that all investors consult with a CPA or accountant for all filing requirements to ensure they comply. Accuplan does not provide any tax or legal advice, and we do not file anything to the IRS except the 5498 and 1099.

Your IRA cannot invest in your own business or a related party’s business because of the disqualified persons rule. We do, however, offer the My Employee Stock Ownership Plan (MYSOP) that would allow this as long as specific guidelines are met through setting up a C Corp and a 401(k).

Stocks and bonds have become the norm. Because of this, most financial advisors and brokers have found ways to make money pushing these products and haven’t broadened themselves outside of these investments. The truth is, most advisors, brokers and custodians just haven’t found a way to make money pushing other types of investments. That is where we come in. We allow you to take full advantage of your IRA by investing in all legally available assets to you.

Yes, you can move your 401(k) into a self-directed IRA, and our rollover process is easy.

Open a Self-Directed IRA With Accuplan

As a self-directed IRA custodian, Accuplan allows investors to invest in a wide range of assets beyond traditional stocks and bonds. Some of the reasons why someone might choose to open a self-directed IRA with us at Accuplan include more investment options, greater control, flexibility, tax advantages, expertise and support.

Open a self-directed IRA with us at Accuplan today.