A traditional IRA at a bank or brokerage provides tax-advantaged growth and access to a standard lineup of stocks, bonds, mutual funds and ETFs. For investors focused on public market exposure, this structure covers the essentials and has done so reliably for decades.

A self-directed IRA operates under the same IRS tax rules and contribution limits but expands what you can invest in. It allows investments in alternative assets, including real estate, private equity, cryptocurrency, precious metals and private lending, provided strict IRS rules are followed and a specialist custodian is involved. The broader access comes with greater responsibility, including more due diligence, documentation and a firm understanding of compliance requirements.

This guide breaks down how these two structures compare so you can determine which aligns with your strategy or whether maintaining both makes the most sense.

Comparing Self-Directed and Traditional IRAs

Understanding the differences between a traditional and self-directed IRA can help you choose between them.

What Is a Traditional IRA?

A traditional IRA is a tax-advantaged retirement account held at a bank, brokerage or robo-adviser. Holdings are limited to publicly traded and pooled products like mutual funds, ETFs, individual stocks, bonds, target-date funds, money market instruments and CDs. Some brokerages narrow this further with proprietary offerings, but the scope stays consistent. Everything on the menu is standardized, liquid and priced daily.

The custodian manages reporting, compliance and recordkeeping. The investor selects from available options, works with an adviser or uses an automated allocation model. For those whose primary goal is diversified market participation with minimal administration, this structure handles the job efficiently.

What Is a Self-Directed IRA?

A self-directed IRA, often called an alternative investments IRA, expands your retirement options beyond stocks and bonds. It operates under the same IRS framework but is administered by a specialist custodian equipped to handle alternative assets. The account holder sources each investment, performs their own analysis and instructs the custodian to execute. Every asset must be titled in the IRA’s name, all income must go into the IRA, and the IRA must pay all expenses.

Standard brokerages lack the infrastructure for real estate closings, metals depository coordination, private equity documentation and cryptocurrency transactions, but specialist custodians exist to support these asset types.

The defining characteristic of an SDIRA is control. You gain access to a significantly wider investment set, and in return, you take on the research, compliance and operational work that accompanies each asset type. For investors with domain expertise in alternative asset classes, this structure allows you to invest for retirement on your own terms.

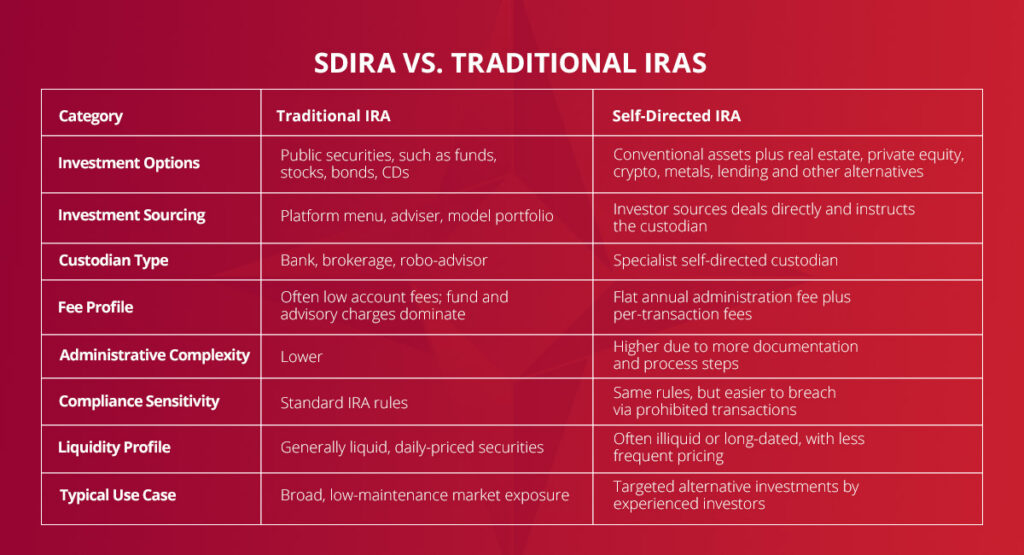

SDIRA vs. Traditional IRAs

| Category | Traditional IRA | Self-Directed IRA |

|---|---|---|

| Investment Options | Public securities, such as funds, stocks, bonds, CDs | Conventional assets plus real estate, private equity, crypto, metals, lending and other alternatives |

| Investment Sourcing | Platform menu, adviser, model portfolio | Investor sources deals directly and instructs the custodian |

| Custodian Type | Bank, brokerage, robo-advisor | Specialist self-directed custodian |

| Fee Profile | Often low account fees; fund and advisory charges dominate | Flat annual administration fee plus per-transaction fees |

| Administrative Complexity | Lower | Higher due to more documentation and process steps |

| Compliance Sensitivity | Standard IRA rules | Same rules, but easier to breach via prohibited transactions |

| Liquidity Profile | Generally liquid, daily-priced securities | Often illiquid or long-dated, with less frequent pricing |

| Typical Use Case | Broad, low-maintenance market exposure | Targeted alternative investments by experienced investors |

How Do Fee Structures Compare?

At a conventional custodian, account-level fees may be low or waived entirely for standard online accounts. The real costs appear in fund or ETF expense ratios and advisory or platform fees, which are typically charged as a percentage of assets under management. For example, a 1% advisory fee on a $500,000 portfolio would be $5,000 annually, and because it is percentage-based, the dollar amount scales directly with your balance.

Self-directed IRAs generally use a more explicit, itemized fee structure. Some custodians charge a flat fee per year regardless of account balance, with transaction fees for specific activities like real estate closings, wire transfers and metals purchases. The base cost stays the same whether the account holds $100,000 or $5 million, which makes a meaningful difference at higher balances.

What Can You Hold in Each Account?

Learn more about what kinds of assets you can hold in each account type.

Traditional IRA

In a traditional IRA, you can hold mutual funds, ETFs, individual equities and fixed-income securities, money market funds, CDs and target-date funds. These are liquid, daily-priced instruments within established regulatory frameworks.

Self-Directed IRA

A self-directed IRA retains access to all conventional securities while adding a broad range of alternatives that most custodians will not or cannot support:

-

Real estate: Real estate investments can include residential rentals, commercial properties, raw land, fix-and-flip projects and syndications. The IRA holds title directly, rental income flows into the account, and every property expense such as taxes, insurance and maintenance must be paid from IRA funds rather than personal accounts.

-

Precious metals: Gold, silver, platinum and palladium that meet IRS fineness standards under IRC 408(m) are qualified investments. These are the only four metals authorized for IRA investment, and storage must be at an approved depository.

-

Cryptocurrency: An SDIRA can hold Bitcoin, Ethereum and other digital assets within the account. Certain specialists can support direct purchase, sale and trading through the account without routing through an external exchange, making the process straightforward once the account is established.

-

Private equity: Investments in private companies, start-ups, venture capital, LLCs and limited partnerships are permitted provided the deal structure does not trigger a prohibited transaction.

-

Private lending: The IRA issues loans via promissory notes and collects interest. The account holder determines note terms, borrower selection and collateral requirements.

-

Tax lien certificates: The IRA purchases the lien, earns interest from the delinquent property owner and may acquire the property if the lien goes unredeemed.

What Neither IRA Can Hold

The IRS prohibits three categories regardless of custodian type — life insurance contracts, S-Corporation stock, and collectibles such as most artwork, rugs, antiques and coins outside narrow statutory exceptions. Beyond those three exclusions, the range of permitted assets is considerably wider than many investors expect, especially with an SDIRA.

SDIRA Pros and Cons

Advantages of a self-directed IRA include:

-

Broadened investment spectrum: An SDIRA offers the flexibility to invest in a wider range of assets beyond traditional stocks and bonds, including real estate, private equity and precious metals.

-

Better investor control: The account holder has direct authority over investment choices, allowing for personalized strategy implementation.

-

Potential for portfolio diversification: Access to alternative assets can help investors build a more diversified retirement portfolio.

Here are some key considerations for a self-directed IRA:

-

Increased management responsibilities: Investors must actively manage due diligence, documentation and operational aspects of their chosen assets.

-

Adherence to IRS regulations: Strict compliance with IRS rules, particularly concerning prohibited transactions, is crucial to maintain the IRA’s tax-advantaged status.

-

Fee structure awareness: It’s important to understand the fee structure, which may include flat annual administration fees and per-transaction charges, potentially differing from traditional IRA costs.

-

Liquidity management: Investors should be mindful that some alternative assets may have longer liquidation timelines, necessitating careful planning for future needs like required minimum distributions (RMDs).

-

Specialized custodian requirement: An SDIRA requires working with a specialist custodian equipped to handle the unique nature of alternative investments.

Who Should Choose a Traditional IRA?

A traditional IRA is well-suited to investors whose primary objective is diversified exposure to public markets without active management. This account type is best for those who prefer low fees and a hands-off approach, as well as investors earlier in their savings journey who benefit from consistent contributions into broad index funds.

It is also the appropriate choice for anyone without specific expertise in alternative asset classes. Real estate, private equity and private lending require specialized knowledge, and a traditional IRA focused on public securities provides a strong foundation without that additional learning curve.

Who Should Choose a Self-Directed IRA?

A self-directed IRA is for investors with direct experience in real estate, private lending, private equity or precious metals who want to put that expertise to work within a tax-advantaged retirement structure. An investor who understands deal structures, property valuations and market cycles brings a level of analysis to IRA-held investments that a passive stock investor would not. The SDIRA allows that knowledge to work for retirement.

This structure also suits investors who have already built a conventional portfolio and want to diversify beyond stocks and bonds. Maintaining a traditional IRA for market exposure alongside an SDIRA for targeted alternatives is a common arrangement. The key requirement is comfort with longer transaction timelines, heavier documentation and strict IRS compliance. If those elements align with how you prefer to operate, an SDIRA gives you the flexibility to invest for retirement your way.

Tax Advantages: Are They the Same?

Yes, the tax advantages are identical. The IRS does not distinguish between a traditional IRA and an SDIRA for tax purposes. Whether it’s traditional or self-directed, a conventional IRA offers tax-deferred growth, and a Roth IRA provides tax-free growth and qualified withdrawals. Contribution limits apply across every IRA an investor holds, combined. Required minimum distributions begin at age 73 for conventional IRAs, but Roth IRAs are not subject to RMDs for the original owner.

The difference between these accounts is what you invest in and how transactions are structured, not how the IRS treats them.

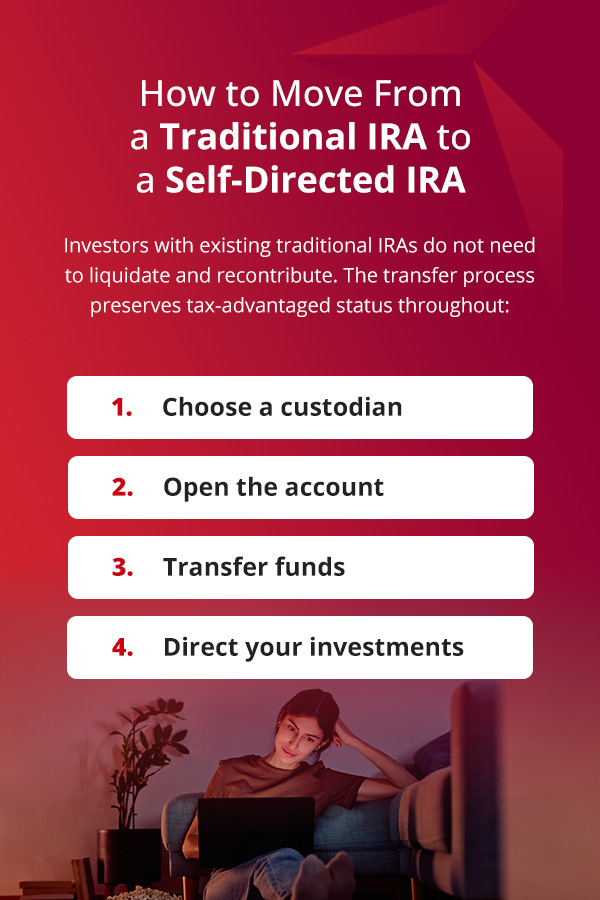

How to Move From a Traditional IRA to a Self-Directed IRA

Investors with existing traditional IRAs do not need to liquidate and recontribute. The transfer process preserves tax-advantaged status throughout:

-

Choose a custodian: Evaluate a potential custodian’s experience with alternative assets, staff tenure and fee structure. Confirm that they support the specific investment types you want.

-

Open the account: Select the appropriate structure — traditional IRA, Roth IRA, SEP, SIMPLE or Solo 401(k) — and open an account.

-

Transfer funds: A direct transfer moves assets from trustee to trustee without triggering taxes or penalties. Most transfers complete within one to three weeks. A 60-day rollover is available but carries risk — miss the deadline and the full amount converts to a withdrawal and you may owe taxes or penalties. Rollovers from 401(k), 403(b) and other qualified plans are also permitted.

-

Direct your investments: Identify the asset, instruct the custodian to execute in the IRA’s name and maintain strict separation between personal and IRA funds throughout.

Both account types can also coexist. Many investors maintain a traditional IRA for market exposure while directing alternatives through an SDIRA. The contribution limit applies across all IRAs combined, but there is no restriction on holding multiple accounts with different custodians.

Common Mistakes to Avoid

-

Prohibited transactions: This is the most consequential compliance area for self-directed IRA holders. IRC Section 4975 prohibits all dealings between the IRA and its “disqualified persons,” including the account holder, their spouse, parents, grandparents, children and grandchildren. Additionally, disqualified persons cannot perform any repairs on IRA assets, even without compensation — this is the sweat equity rule.

-

Self-dealing rule: The IRA cannot purchase property that the account holder already owns, and the account holder cannot live in or use IRA-held real estate. Even paying an IRA expense from personal funds with the intention of reimbursing yourself from the IRA is a violation. Engaging in prohibited transactions or self-dealing can cause the IRS to treat the entire IRA as distributed on January 1 of the violation year, with a 10% penalty if under 59½.

-

Underestimating total costs: The flat annual fee is competitive at higher balances, but transaction fees for closings, wire transfers and metals purchases accumulate. Model the complete cost picture across anticipated transactions before committing.

-

Liquidity gaps: IRA-owned real estate is difficult to liquidate on short notice, and private equity may carry multiyear lock-up periods. Adequate liquid reserves inside the account are essential for covering RMDs, ongoing expenses and unexpected costs.

-

Skipping due diligence: The custodian administers the account but does not evaluate investment quality. That responsibility rests with the account holder. Every alternative asset requires independent analysis before instructions go to the custodian.

-

Excessive conservatism in a traditional IRA: Allocating entirely to cash equivalents or ultra-conservative positions when decades of growth remain limits long-term compounding. Traditional IRAs provide access to diversified equity and fixed-income funds — investors should use the full range available to them.

Frequently Asked Questions

Here are the answers to some common questions about IRAs:

Can I Hold Both a Traditional IRA and a Self-Directed IRA?

Yes. The IRS contribution limits apply to the combined total across all IRAs, but there is no restriction on maintaining multiple accounts at different custodians simultaneously.

Can I Set up an LLC in My Self-Directed IRA?

Yes. An IRA LLC allows the account holder to act as manager of an LLC wholly owned by the IRA. You control transactions from an LLC bank account rather than routing each one through the custodian, which is extremely useful for frequent or time-sensitive purchases. Tax treatment remains the same, and all prohibited transaction rules still apply.

Is a Solo 401(k) the Same as a Self-Directed 401(k)?

They are the same structure. A solo 401(k) and a self-directed 401(k) are synonyms, designed for self-employed individuals and small business owners with no full-time employees other than a spouse.

Take the Next Step With Accuplan

Accuplan Benefits Services has administered Self-Directed IRAs since 2007, with retirement industry experience dating to 1985. Our team members average over 15 years with the company and have decades of hands-on experience with self-directed accounts. We administer traditional and Roth self-directed IRAs, solo 401(k) plans, SEP IRAs, SIMPLE IRAs and HSAs across real estate, precious metals, cryptocurrency, private equity and private lending. Call us at 888-443-9609, open an account online in minutes or request more information to get started.

Our information shouldn’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.