Individual Retirement Accounts (IRAs) have rules stating what you can and cannot do with your retirement savings. For instance, with a traditional IRA, you’ll be charged a 10% early withdrawal penalty if you take distributions before you’re 59 ½ years old unless an exemption applies. In addition to the 59 ½ rule, Roth IRAs also have a five-year rule, meaning you can’t withdraw earnings until five years after your first contribution. A self-directed IRA (SDIRA) lets you invest in real estate, but you also can’t engage in self-dealing transactions. Failing to comply risks your IRA’s tax-advantaged status.

However, the IRS also allows certain exemptions, such as an IRA withdrawal for a home purchase. If you plan to buy a house for personal or business use, this article outlines the guidelines you need to follow and when it makes the most financial sense to make the purchase.

Can You Use Your IRA to Buy a House?

You can use your traditional or Roth IRA funds to buy a home through the first-time homebuyer exemption. However, you can also purchase a house as a real estate investment through an SDIRA. The IRS rules govern both instances.

What Is the First-Time Homebuyer Exemption?

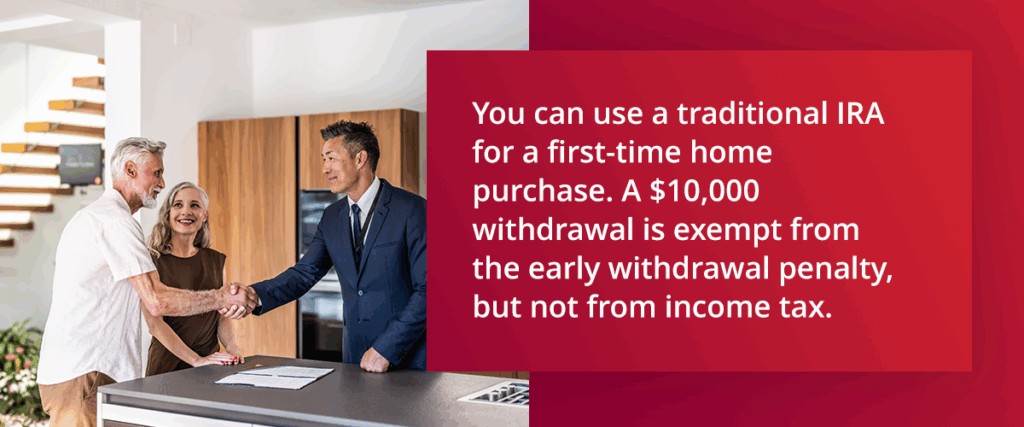

The first-time homebuyer IRA exemption lets you take a distribution of up to $10,000 to help pay for your home. If you have a traditional IRA, you won’t pay the 10% early withdrawal penalty, but you still need to pay income tax. You must use the funds for qualified acquisition costs, which include:

- The cost of purchasing, building or rebuilding the house.

- Typical and reasonable settlement, financing and closing costs.

To be considered a first-time homebuyer, you must not have owned a home in the past two years. This means if you owned and sold a house five years ago, you can still claim the $10,000. This is a lifetime limit, meaning you can claim it only once. It’s also applicable per person, so you and your spouse can each take a distribution in your IRAs, totaling a $20,000 withdrawal. Your spouse must also be a first-time homebuyer.

You can use the funds for yourself or for family members, such as your child, grandchild or parent, who need help paying for their home — provided they’re paying for qualified acquisition costs. Your family members must also qualify as first-time homebuyers.

You must use the funds within 120 days. If the deal gets delayed or falls through, you can contribute the funds back to your IRA within the 120-day period. You won’t be charged the early withdrawal penalty. The contribution is treated as an IRA rollover, even though the usual window for IRA rollovers is 60 days. The one-rollover-per-year rule also does not apply.

How to Purchase a House Using Your IRA

An IRA withdrawal can have tax implications, depending on your account type. When purchasing a house using IRA funds, remember the following:

Using a Traditional IRA

Traditional IRA contributions are made with pretax dollars, while earnings grow tax-free. You’ll only be taxed when you take a distribution. Even when using the first-time homebuyer exemption, your distribution is subject to income tax. Your withdrawal can comprise both earnings and contributions. Only $10,000 qualifies for the first-time homebuyer exemption. Above this limit, you’ll be subject to the 10% early withdrawal penalty on top of the income tax if you’re younger than 59 ½.

When claiming the exemption, you must prove your and your spouse’s eligibility. You should also keep records showing that you’ve used the funds for qualifying acquisition costs and the contract showing the acquisition date. The IRA custodian will issue Form 1099-R, so you can report the distribution on your tax return. The form indicates the nature of the distribution, including any applicable exemptions.

Using a Roth IRA

The home purchasing rules for a Roth IRA are the same as those for a traditional IRA, but the tax treatment differs. Since you make Roth IRA contributions with after-tax dollars, you typically don’t have to pay income tax upon withdrawal.

Withdrawal for Roth IRAs follows a specific order:

- Contributions

- Conversions or rollovers

- Earnings

You cannot withdraw earnings until you’ve withdrawn your contributions, and then the amounts rolled over. Rollovers are funds you roll over from another IRA into your Roth IRA. You can withdraw contributions tax-free and penalty-free any time. However, you need to wait for five years, from the beginning of the year you made your first contribution, before you can withdraw earnings tax-free. The five-year clock for the conversions is a separate five-year period.

The IRA custodian will issue the same Form 1099-R for Roth IRAs.

Using an SDIRA

Compared to a standard IRA, SDIRAs let you invest in alternative assets, including real estate, private businesses and precious metals. SDIRAs can also be a traditional or Roth IRA. However, unlike standard IRAs managed by financial institutions, you’re in charge of the investment decisions with an SDIRA. You’ll still be working with a custodian to whom you’ll direct your investment decisions.

SDIRAs also follow IRS rules, including the prohibition on self-dealing activities. You can’t engage in business transactions that benefit you or your family, such as purchasing your primary residence. However, you can buy a house to use as a rental property.

An SDIRA for real estate is also known as a Real Estate IRA. The IRS sets the annual contribution limits, which are the same as those of a standard IRA. The IRA will own any property you purchase, so all income and expenses must flow through the account.

You can purchase a property once your SDIRA has enough funds. However, your SDIRA can also partner with investors, such as yourself, for the purchase. After the purchase, the IRA cannot conduct transactions with disqualified persons, including you and your family members. The ownership, expenses and profits are divided according to investor contributions.

Looking at real estate as an investment instead of a primary residence? A Self-Directed IRA can hold rental property, raw land or commercial real estate, with rental income flowing back into the retirement account tax-deferred (or tax-free in a Roth). See how the Real Estate IRA works.

Traditional vs Roth vs Self-Directed IRA: Side-by-Side

The three IRA paths to a home purchase are not interchangeable. The first two pull cash out of the retirement account so you can buy a personal residence. The third keeps the money inside the IRA and the IRA itself owns the property as an investment.

Pull cash from your IRA

- Tax on the withdrawal

- Traditional: taxed as ordinary income. Roth: contributions come out tax-free anytime; earnings are tax-free only if the Roth has been open at least five years.

- Penalty on the first $10,000

- Waived under the first-time homebuyer exception. Applies to both Traditional and Roth.

- How the property can be used

- Personal residence. You own the house, not the IRA.

- Best fit

- First-time buyer who needs help with the down payment.

Hold real estate inside a Self-Directed IRA

- Tax on the withdrawal

- No personal withdrawal. The IRA owns the property. Rent and gains flow back into the IRA, tax-deferred if Traditional or tax-free if Roth.

- Penalty on the first $10,000

- Not applicable. No distribution is taken.

- How the property can be used

- Rental or investment property only. Never your residence or a family member's.

- Best fit

- Investor who wants real estate inside the retirement account.

A few rules apply across all three paths. The first-time homebuyer exception caps at $10,000 per person across your lifetime, so a married couple where both qualify can withdraw $20,000 combined (source). Self-Directed IRA purchases must be at arm’s length from you and your family; the property cannot be your residence, your vacation home or rented to a disqualified person (source).

Is Using Your IRA to Buy a House a Good Idea?

Using your IRA to purchase a house can be a good idea, depending on your circumstances. Consider the following benefits and drawbacks:

Benefits of Using Your IRA to Buy a House

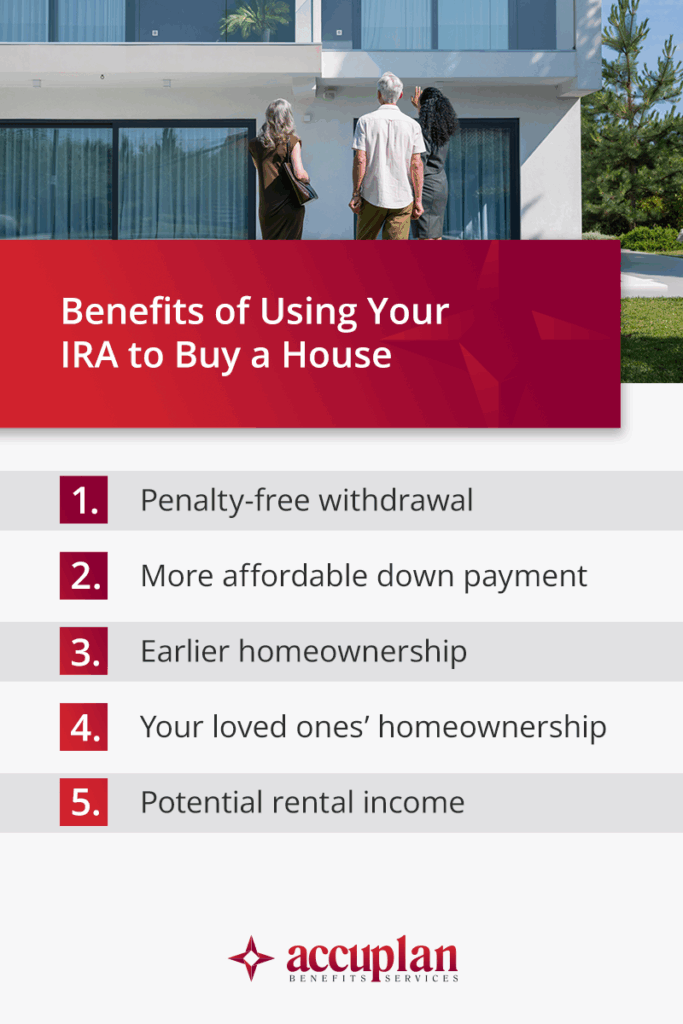

Using your IRA funds for purchasing a house lets you enjoy:

- Penalty-free withdrawal: You don’t need to wait for retirement or until you’re 59½ years old to take distributions and buy a home. The penalty-free withdrawal can be a significant amount, especially if you purchase a house with your spouse.

- More affordable down payment: Instead of paying the cost of down payment with your pocket money, you can use your retirement savings — especially if you plan to use the home throughout retirement.

- Earlier homeownership: Saving up for a house can take time. You can use the money you already have in an IRA to stop renting and start owning a home.

- Your loved ones’ homeownership: If you don’t need the $10,000 exemption for yourself, you can help out a family member in purchasing their home. This can be a great way to help out your child or parent, for instance, in achieving a personal milestone.

- Potential rental income: Using an SDIRA to purchase a rental property means you can enjoy additional income, which can benefit you through retirement.

Drawbacks of Using Your IRA to Buy a House

Taking money from your retirement savings comes with the following downsides:

- Reduced retirement savings: The most obvious downside is the reduction in your retirement savings. This can require significant replanning of your retirement goals if you’re nearing your targeted retirement age.

- Potential income taxes: Your distribution from a traditional IRA is subject to income taxes. This can reduce your spending capacity when buying a home.

- Limited exemption: The amount you’ll receive is up to $10,000 only — $20,000 if both you and your spouse are first-time homebuyers. This amount may be lacking depending on the property you’re purchasing. You may also feel additional pressure when selecting a home due to the lifetime limit.

- IRS rules and consequences: Whether you’re using a standard IRA or an SDIRA, IRA rules apply, which can be tricky to understand. However, failing to comply can lead to costly consequences, including penalties. For instance, a prohibited transaction can cost you 15% of the amount involved. Failing to correct this transaction results in an additional tax that is 100% of the same amount.

When It Makes Financial Sense

In some instances, an early IRA withdrawal may be advantageous. However, consider carefully how it affects your long-term goals. Using IRA funds to purchase a house can make sense if:

- The $10,000 IRA withdrawal exemption for first-time homebuyers offers financial relief: If you’re tight on budget and purchasing a home is key to your goals, the exemption can be worth it.

- You’re purchasing a retirement home: Since you can only claim the exemption once, consider using the $10,000 for a house you can see yourself living in long term — for instance, if you see the house as your forever home where you’ll retire.

- You can withdraw Roth IRA earnings tax-free: You might not have contributions worth $10,000. If you’ve made your first contribution five years ago, you can withdraw your earnings tax-free, which can fill the $10,000 amount.

- You can afford to reduce your retirement savings: If you’re on track with your retirement goals and have excess funds, then you can claim the exemption without having to restrategize for retirement.

- You’re eyeing a profitable property for your SDIRA: The potential earnings of a rental property can negate the downside of reducing your retirement funds. The property can also remain as a source of income throughout your retirement.

How to Rebuild Your Retirement Savings After an IRA Withdrawal

If you decide to push through with the early withdrawal, it’s possible to rebuild your retirement savings with proper planning. The right strategy depends on where you’re at with your goals. Here’s what you can do to get back on track:

- Assess your progress: To rebuild your savings, understand the impact of your early withdrawal and how it affects your financial situation. Do you have to change your retirement age? Do you need to adjust your monthly savings? Consider using rules of thumb to provide an estimate.

- Create an updated, realistic budget: After analyzing where you’re at financially, create an updated plan that will put you back on track with your goals. Consider whether you need to reduce your expenses. You may also maximize your employer benefits, if you have them. For instance, if your employer matches your contributions, consider maximizing these contributions to boost your retirement savings.

- Leverage your home’s equity: Home equity refers to the portion of your home that you own outright. You get this by subtracting the outstanding mortgages from your home’s market value. While fully paying off the mortgage provides a sense of financial freedom, it can also help you leverage your home’s equity during your retirement by selling or renting the home to someone else.

Frequently Asked Questions

Can I use my Roth IRA to buy a house without penalty?

Yes. Your own Roth contributions can come out at any time, for any reason, tax-free and penalty-free. Earnings are more restrictive. To withdraw earnings tax-free for a first-home purchase, the Roth account must be at least five years old and you must qualify as a first-time homebuyer. The lifetime limit on earnings used this way is $10,000. See the IRS guide to Roth IRA distributions.

How much can I withdraw from my IRA for a first home purchase?

The first-time homebuyer exception caps the penalty-free withdrawal at $10,000 per person across your lifetime. A married couple where both qualify as first-time buyers can withdraw $20,000 combined. Any amount above the cap is subject to the 10% early-withdrawal penalty if you are under 59 ½. See the IRS guide to IRA distributions.

What is the 5-year rule for Roth IRA home purchases?

The five-year clock starts on January 1 of the year you made your first Roth contribution. After five tax years, qualified withdrawals of earnings, including the $10,000 first-time homebuyer amount, come out tax-free. Before the five years are up, the earnings portion is still taxable as income, even though the 10% early-withdrawal penalty is waived under the first-time homebuyer exception. See the IRS guide to Roth IRA distributions.

Can I use an inherited IRA to buy a house?

The first-time homebuyer exception applies differently for a non-spouse inherited IRA. Non-spouse beneficiaries follow the 10-year payout rule and pay income tax on Traditional IRA distributions, though distributions are generally not subject to the 10% early-withdrawal penalty regardless of the beneficiary’s age. Talk to a tax advisor before pulling funds from an inherited account. See the IRS guide to inherited retirement accounts.

What’s the difference between using a Traditional IRA vs a Self-Directed IRA for real estate?

A Traditional IRA distribution puts cash in your hand, and the first-time homebuyer exception waives the early-withdrawal penalty on up to $10,000 that you use toward a personal residence. A Self-Directed IRA works the opposite way. The IRA itself buys, owns and rents the property as an investment, and you cannot live in it or let a disqualified person such as a spouse, parent or child use it. The Traditional path funds a personal home. The Self-Directed path funds a rental held inside the retirement account. See the IRS rules on prohibited transactions.

Why Trust Accuplan Benefits Services

Accuplan Benefits Services has been helping clients since 1985, empowering them to grow their retirement savings to their fullest potential. The IRS rules can be overwhelming and specific, especially for SDIRAs. Certain assets also have particular rules. With the help of our extensive industry knowledge, clients don’t need to navigate these rules on their own and risk having their accounts disqualified.

We’ve been administering over 10,000 accounts with more than 40,000 investments, worth over $1.5 billion. Apart from real estate, our clients also invest in private equity, precious metals, cryptocurrencies and other alternative assets. If you’re planning to buy a house with an SDIRA, we can help you out.

Invest in a House Through Your SDIRA With Accuplan

Whether you have an SDIRA or a standard Roth and Traditional IRA, withdrawal penalties can be costly. Misunderstanding the rules and unintentionally engaging in prohibited transactions can also risk your IRA’s tax-advantaged status. SDIRA rules can be tricky to navigate on your own, and we understand that they can get complex. This is why we’re here to help — we’ll guide you through the process and offer the support you need.

With an SDIRA, you can purchase a rental property, vacation home or other real estate investments. It can be an alternative way to make your savings work for you, instead of leaving them in a retirement savings account. Unlike the IRS rules, our application process is simple and convenient. Fill out an application today to get started.

**Disclaimer: **Our information shouldn’t be relied upon for investment advice but simply for information and educational purposes only. It is not intended to provide, nor should it be relied upon for accounting, legal, tax or investment advice.

Ready to start?

Open a self-directed IRA today.

10-minute application. Real human support.